Robinhood's Layoff Rally Prices Efficiency, Not Distress

Robinhood's layoff news did not trade like distress. HOOD rose 8.8% after the company announced a 10% workforce reduction, while the company filing said the cut involved approximately 10% of full-time employees and a small number of open roles.

Job cuts do not create value by themselves. Robinhood said it was acting from a position of business strength, with June month-to-date average daily trading volumes at record levels across equities, options and prediction markets. That framed the repricing around a narrower question. Can a smaller organization ship faster while customer activity remains strong?

Source - Robinhood Form 8-K dated June 16, 2026. Asset scope is Robinhood Markets restructuring charge components, date range Q2 2026, interval company filing, basis company-estimated charges.

The filing made speed the primary catalyst

Framing drove the primary catalyst. The SEC filing says the reduction was part of efforts to maintain a high performance culture, accelerate product velocity and remain lean and disciplined.

For fintech stocks, layoffs normally raise demand concerns. Here, Robinhood put product velocity and record trading intensity in the same filing as the workforce reduction. The market got an efficiency signal before it got detailed savings guidance.

Disclosure risk sits inside the same filing. Robinhood warned about workforce-management difficulty, declining or negative growth, legal, reputational and financial effects, and possible operational disruptions from the reduction. If those risks show up, the efficiency label was premature.

May metrics made the strength claim harder to dismiss

May data gave the strength claim an operating base. Robinhood reported 27.7 million funded customers, up about 1.76 million year over year, and $377 billion of platform assets, up 48% year over year.

Activity was broad enough to matter. The same release showed $315 billion of May equity notional volume, up 75% year over year, 231 million options contracts, up 29%, 3.9 billion event contracts, up 22% from April, and $19.5 billion of margin balances, up 117% year over year.

Company monthly figures were still a basis, not a victory lap. Robinhood said the May operating figures were unaudited and preliminary for months in the most recent fiscal quarter. Even with that caveat, they explain why the layoff did not read as a simple demand-collapse signal.

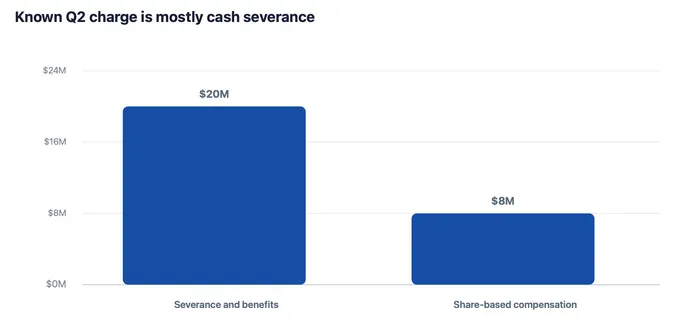

The charge was visible while savings were not

Cost appears before benefit. Robinhood estimated about $20 million of cash restructuring charges for employee severance and benefits and about $8 million tied to share-based compensation, with recognition expected in the second quarter of 2026.

Here, the chart matters because it establishes the near-term charge and its mix. It does not establish that product velocity improves, costs stay lower, or revenue momentum absorbs the disruption.

A disciplined thesis separates the known cost from the hoped-for productivity gain. The constructive read is leaner execution into high activity. The failure case is that cuts add friction just as Robinhood is trying to widen the platform and push newer product lines.

The operating-leverage case now has to show up in speed

Q1 already made product velocity the budget story. Robinhood said its 2026 expense plan was designed to accelerate product velocity, drive net deposit growth and grow revenues, while updated 2026 adjusted operating expenses and share-based compensation guidance stood at $2.7 billion to $2.825 billion and excluded restructuring charges.

Operating leverage depends on that link. If headcount is lower and product velocity stays high, revenue tied to trading activity, margin balances and platform assets has more room to flow through after the Q2 charge.

Lower coordination can help, but the mechanism is not automatic. Fewer employees can reduce coordination layers, but it also raises the execution burden on remaining teams. For HOOD, the question is whether the company can keep broad activity while asking a smaller workforce to move faster.

The validation is volume durability and expense follow-through

Next, June volumes have to do more work. June volumes must keep supporting the record-activity claim, May customer-asset momentum has to carry through quarter close, and management has to show whether the Q2 charge leads to visible expense discipline rather than one more adjustment.

A strong follow-through would support the market's view that this was an efficiency reset. Weak volumes, slower net deposits, product delays or restructuring disruption would shift the same news back toward execution risk.

For HOOD, the reward came from pairing cuts with activity evidence. The signal lasts only if June volumes, net deposits, margin balances and product cadence back the leaner-cost story in Q2 updates.