No Hike, No Forward Guidance: The Warsh Fed Begins With A Market Selloff

The Fed held rates steady but removed forward guidance, triggering a market selloff as investors priced in potential hikes and heightened policy uncertainty.

The Federal Reserve did exactly what investors expected on rates. The market reaction showed that almost everything else was a surprise.

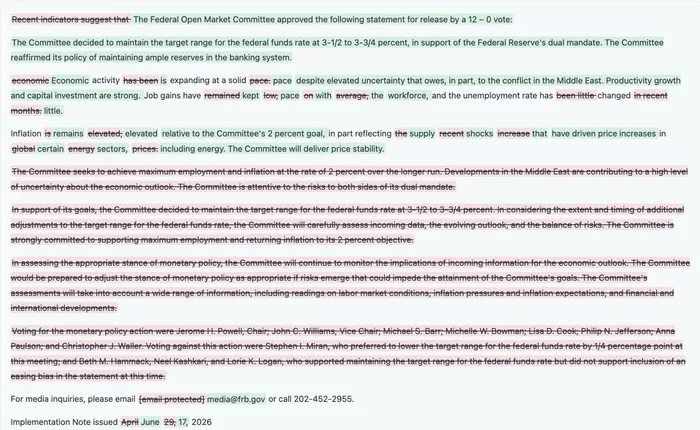

At Kevin Warsh’s first meeting as Fed chair, the FOMC unanimously kept the federal funds rate unchanged at 3.50% to 3.75%, marking the fourth straight meeting without a move. But the statement, projections and press conference all pointed in the same direction: the Fed is no longer preparing markets for easier policy. It is preparing them for less guidance, more uncertainty and possibly higher rates.

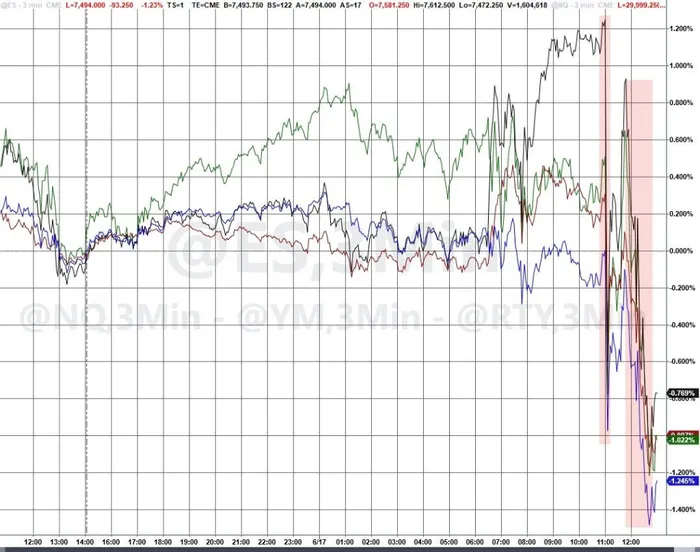

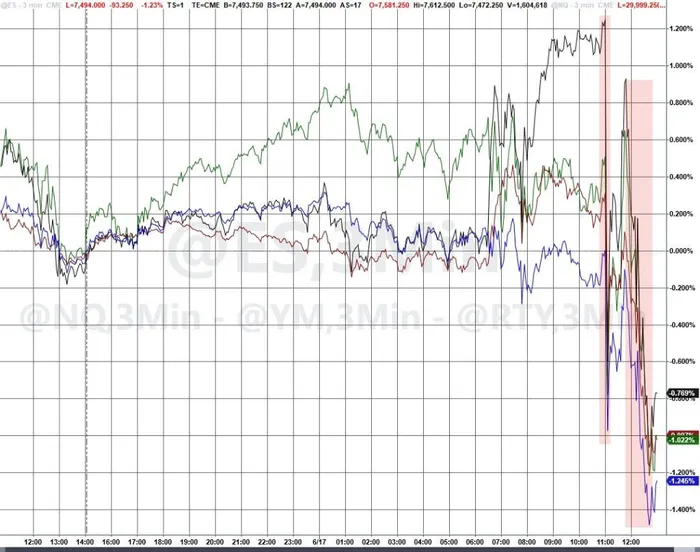

US stocks initially rose after the rate decision, then reversed sharply as investors absorbed the hawkish message. The Nasdaq fell 1.34%, the S&P 500 dropped 1.21%, and the Dow lost 0.97%. Precious metals were hit even harder: spot gold fell 1.71% to $4,257.37, while spot silver dropped 3.01% to $67.92.

The Hold Was Expected. The Communication Shift Was Not.

The biggest change was not the rate decision itself. It was the way the Fed chose to communicate.

Under Warsh, the policy statement was sharply shortened, reportedly from more than 300 words to just over 130 words. More importantly, the Fed removed traditional forward-guidance language that markets had long used to infer the likely path of interest rates.

That is a major regime shift.

In the Powell era, investors often treated the statement, dot plot and press conference as a roadmap. Even when the Fed claimed to be data-dependent, markets could usually extract a bias: cut, hold or hike.

Warsh appears to want the opposite. His first statement gave fewer clues, not more. He also suggested that forward guidance is less useful in the current environment, where inflation, energy prices and geopolitical risks are moving quickly.

For traders, this means the Fed may become harder to forecast. Market pricing could react more violently to every inflation report, jobs number and Warsh press conference because the central bank is no longer offering the same level of advance signaling.

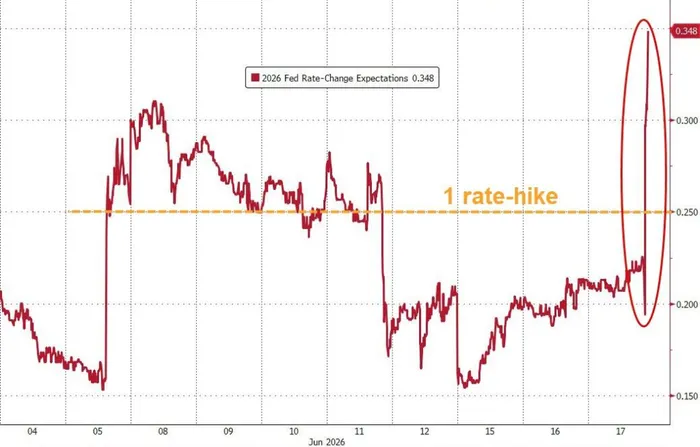

The Dot Plot Turned Hawkish, But Warsh Refused To Join It

The second shock came from the dot plot.

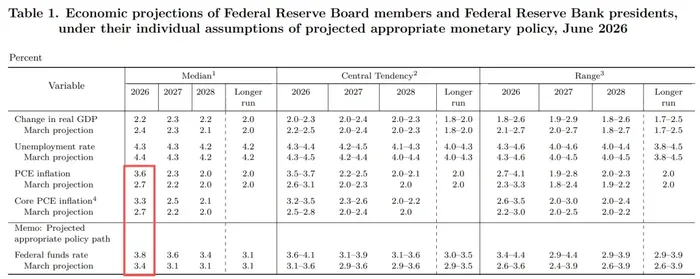

Warsh himself declined to submit economic and rate projections, reinforcing his long-running skepticism toward the dot plot as a policy tool. But among the remaining officials, the message was clearly more hawkish than before.

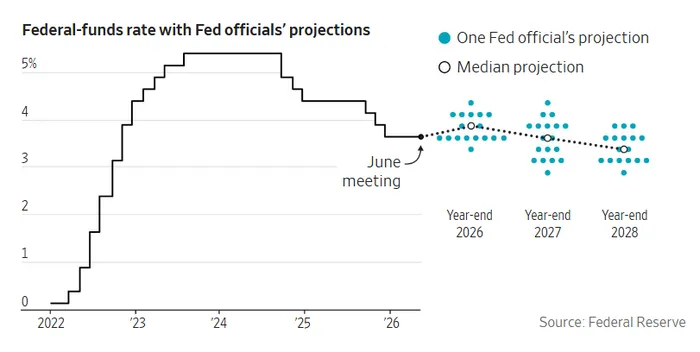

Of the 18 officials who submitted projections, nine now expect at least one rate hike by the end of 2026. Six expect at least two hikes. In March, no official had projected a rate hike this year.

That shift was enough to change the market’s interpretation of the entire meeting. A steady-rate decision suddenly looked less like a pause before cuts and more like a pause before possible tightening.

The Fed’s economic projections also moved in a more inflation-focused direction. Officials raised their inflation expectations while keeping the labor-market picture relatively stable. That combination matters: if inflation is the main problem and employment is not deteriorating quickly, the Fed has less reason to cut and more room to stay restrictive.

Warsh’s own message was similarly firm. He emphasized that the FOMC is committed to returning inflation to 2%, while avoiding a clear promise about the next move.

In plain English, the Fed did not hike yesterday. But it made sure markets understood that hikes are back on the table.

Why Stocks And Metals Sold Off Together

The market reaction was classic hawkish Fed pricing.

Stocks fell because higher-for-longer rates pressure valuations, especially in growth sectors that depend on future earnings. If the Fed may still raise rates this year, equity investors need to apply a higher discount rate to future profits.

Gold and silver fell for a different but related reason. Precious metals are highly sensitive to real rates and the dollar. When the market prices in a greater chance of rate hikes, yields tend to rise and the dollar strengthens. That makes non-yielding assets such as gold and silver less attractive in the short term.

This is why the selloff in metals was so sharp. Gold had previously benefited from geopolitical risk, inflation fears and expectations that the Fed would eventually ease. Warsh’s first meeting challenged the last part of that trade.

The key market takeaway is not that the Fed has already restarted a hiking cycle. It has not. The key point is that inflation concerns are now the dominant message again.

For investors, the Warsh Fed may be less predictable than the Powell Fed, but not necessarily less hawkish. The central bank is saying less, while worrying more about inflation. That is a difficult combination for markets that had grown used to reading the Fed like a script.

The next few inflation reports may now matter more than the next Fed statement. If price pressures cool, markets can still recover quickly. But if inflation remains sticky, Warsh’s shorter, less-guided Fed may leave investors with fewer warnings before the next policy surprise.