MSTR's ATM Engine Is Outrunning Its Bitcoin Buys

Strategy sells shares to fund bitcoin, but rising reserves and financing costs dilute per-share value, pressuring MSTR stock despite continued accumulation.

Strategy is still buying bitcoin, but MSTR is being marked down for the way those purchases are funded. Investor's Business Daily reported that MSTR fell 5.1% to $116.56 on June 17 while bitcoin traded around $64,400, after two SEC updates showed Strategy sold $390.0 million of common stock over two weeks while buying $201.3 million of bitcoin.

A simple accumulation story is getting harder to defend. The filings still show ATM-funded bitcoin purchases, but they also show a rising USD Reserve and a market source focused on financing obligations. For MSTR, the repricing object is no longer only how many coins Strategy adds. It is whether common-stock issuance still protects bitcoin per share.

Source - multiple SEC filings. Source scope is Strategy June 8 8-K and Strategy June 15 8-K, with links to June 8 filing and June 15 filing. Asset scope is MSTR common-stock ATM net proceeds and Strategy bitcoin purchase amounts, date range June 1 to June 14, 2026, interval weekly filing periods, basis net proceeds and aggregate purchase price inclusive of fees and expenses.

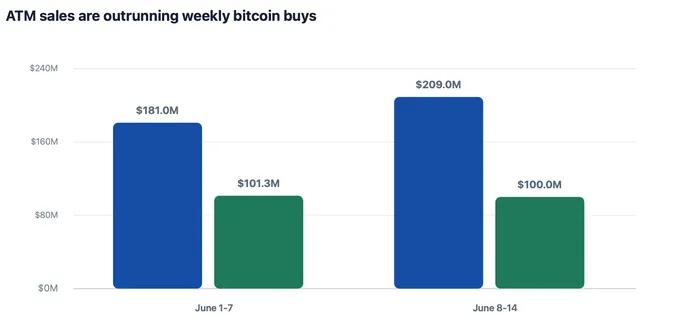

Common stock sales funded more than bitcoin purchases

The latest filing shows the gap. Strategy said it sold 1,732,553 MSTR shares during June 8 to June 14, raising $209.0 million of net proceeds, while it acquired 1,587 bitcoin for $100.0 million.

One week earlier, Strategy had sold 1,409,600 MSTR shares for $181.0 million of net proceeds and acquired 1,550 bitcoin for $101.3 million. Purchase size stayed near $100 million while common-stock proceeds increased.

That does not mean the bitcoin purchases stopped mattering. It means the funding channel has a different analytical job. Cash raised through common stock now has to be judged against coins acquired, reserve needs and financing cost, not just against the headline number of bitcoin added.

The reserve turns dilution into a balance-sheet signal

Reserve-building explains part of the market concern. Strategy reported a $1.0 billion USD Reserve as of June 7 and a $1.1 billion USD Reserve as of June 14, including expected ATM proceeds not yet settled.

IBD put that reserve into the near-term financing frame. The report said Strategy faces about $230 million of interest and dividend payments due at the end of June and wants to rebuild the reserve to at least $2.25 billion from $1.1 billion.

A larger reserve can reassure preferred and debt holders, so the cash is not wasted by definition. For common shareholders, though, every dollar retained for obligations is a dollar that did not immediately become bitcoin exposure.

Buying power is tied to the premium, not only bitcoin

MSTR's financing math depends on the stock's premium to its bitcoin holdings. IBD said current MSTR and bitcoin prices left Strategy shares about 20% below the level needed to finance bitcoin purchases without reducing bitcoin per share.

Scale cuts both ways. Strategy reported 846,842 bitcoin as of June 14, with an aggregate purchase price of $64.07 billion and an average purchase price of $75,656. A balance sheet that large makes every funding decision visible.

The counterpoint is straightforward. A bitcoin rally or a recovery in MSTR's premium could restore more favorable issuance math. Without that recovery, common-stock sales can add coins while still weakening the per-share story.

Preferred stock kept the funding stack complicated

Preferred financing is not providing the same release valve. IBD said the STRC preferred dividend rate would likely rise from 11.5% to at least 11.75%, and potentially 12%, if volume-weighted pricing remained weak.

The June 15 filing reinforces why common stock mattered that week. The ATM table showed no STRF, STRC, STRK or STRD preferred stock sold during June 8 to June 14, leaving MSTR common stock as the active issuance line in the filing.

Capacity still exists. Strategy listed $25.7468 billion of MSTR stock available for issuance and sale as of June 14. Shelf capacity is present, but market tolerance for more common-stock dilution now decides how much weight the bitcoin-per-share argument can carry.

The next ATM update becomes the validation point

The next weekly filing has to answer a narrow question. Does fresh issuance mainly fund more bitcoin, or does a larger share continue moving toward reserve repair and financing obligations?

A stronger update would show a healthier balance among ATM proceeds, bitcoin purchase size, reserve needs and preferred costs. Another week of large common-stock sales with limited bitcoin buying would keep the pressure on MSTR's premium.

A publishable next update would narrow the gap between common-stock proceeds and bitcoin purchases, hold the reserve path steady and keep preferred costs contained. Without that mix, MSTR remains exposed to financing pressure even if Strategy keeps adding bitcoin.