Micron Earnings Face an 81% Margin Bar After a 260% Rally

Micron Technology will report fiscal third-quarter results after the Nasdaq close on Wednesday, June 24, with MU last closing at $1,133.99 on June 18. That close was roughly 260% above January 2, far ahead of the 104% gain in SOXX over the same close-to-close window.

Such a run changes the earnings burden. Management already set an exceptional baseline of $33.5 billion in revenue, about 81% non-GAAP gross margin and $19.15 in non-GAAP EPS at the midpoint. A modest beat may confirm the June quarter without answering whether pricing and margins can remain elevated into fiscal 2027.

A routine beat would not clear the new earnings bar

Recent public previews place Q3 revenue around $33.7 billion to $34.0 billion and non-GAAP EPS around $19.2 to $19.4. Those ranges sit only slightly above management's midpoints, which means a small headline beat would mostly confirm expectations that have already moved higher.

Year-over-year growth will look spectacular because fiscal Q3 2025 revenue was $9.30 billion and non-GAAP EPS was $1.91. That comparison explains the earnings acceleration, but it does not decide the stock's next phase. MU now carries a forward burden after its 2026 outperformance, and the first Q4 guide will reveal whether estimate revisions still have room to rise.

A softer number would not automatically end the cycle if it reflects shipment timing. Still, weaker Q4 pricing or a lower margin guide would carry more information than a small Q3 miss because the multi-year shortage view depends on the earnings base staying unusually high.

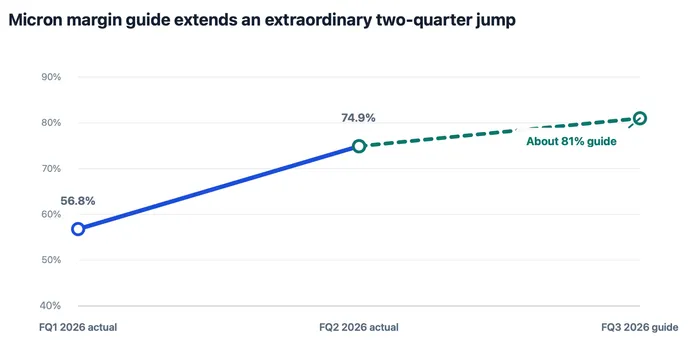

Gross margin carries the cycle argument

Micron's non-GAAP gross margin moved from 56.8% in fiscal Q1 to 74.9% in fiscal Q2, and management guided to approximately 81% for Q3. Revenue measures the size of the upcycle, while margin shows whether tight supply and richer product mix are converting into earnings power.

FQ1 and FQ2 are reported non-GAAP gross margin. FQ3 is company guidance, not an actual result.

Provider Micron Technology. Symbol MU. Date range FQ1 2026 through FQ3 2026 guidance. Interval fiscal quarter. Basis non-GAAP reported gross margin and company guidance.

An 81% margin can support another large EPS step, but it can also mark the point where comparisons become hardest. Q4 commentary must separate durable HBM-led mix and broad DRAM pricing from a shortage peak that begins to ease as capacity and customer inventories adjust.

Institutional forecasts depend on a supply gap lasting years

Deutsche Bank presents the most aggressive public case. Its June view reportedly models about $160 of fiscal 2027 EPS, gross margin above 80% and a supply imbalance lasting into 2028. HBM demand sits at the center of that argument because it consumes wafer capacity that might otherwise serve broader DRAM demand.

Other institutional checks point in the same direction over a shorter horizon. Rosenblatt sees new wafer supply about 12 months away, while Wedbush expects roughly 20% Q3 pricing gains for DRAM and NAND. These are secondary forecasts rather than company guidance, but they explain why a merely solid quarter may not satisfy the assumptions now embedded in MU.

Every version of the bullish case shares a fragile premise. New capacity must arrive slowly enough, and AI-server demand must remain strong enough, to prevent customer inventories from rebuilding ahead of use. Earlier supply, weaker cloud capital spending or price resistance would pull the story back toward a familiar memory peak.

Free cash flow separates pricing power from expansion costs

Fiscal Q2 generated $11.90 billion of operating cash flow, $5.0 billion of net capital expenditures and $6.9 billion of adjusted free cash flow. Those figures show that stronger pricing is reaching cash even after a heavy investment quarter.

Capital discipline remains central because supply scarcity eventually attracts new supply. Micron's June 10 selection of Bechtel for its New York semiconductor project reinforces the long construction runway behind future domestic capacity. The project does not change near-term Q3 output, but it shows why the upcycle cannot be judged from gross margin without tracking capital spending.

Q3 adjusted free cash flow should therefore move with the margin expansion, while Q4 capex will indicate how much of that cash Micron plans to commit before new fabs contribute bit supply. Strong cash generation with measured spending would support the longer-cycle case. A faster capital ramp without a matching demand outlook would narrow the cushion.

A softer fourth-quarter guide would expose the rally burden

MU can absorb a small Q3 variance if Q4 guidance keeps gross margin near the current level and management supports pricing with customer demand and constrained supply. The 260% rise through June 18 means the stock is less dependent on the reported quarter than on the duration of earnings above prior-cycle norms.

A lower forward margin, signs of customer inventory accumulation or faster wafer additions would weaken that duration case. Conversely, another strong revenue guide paired with stable margin and free cash flow would give the institutional forecasts a firmer operating base without turning them into company facts.

The most useful disclosures on June 24 will be Q4 revenue and gross-margin guidance, HBM allocation, DRAM pricing, capital expenditures and adjusted free cash flow. Together they will show whether the June quarter is the top of an extraordinary cycle or the base of a longer one.