Carnival's 5% Drop Shifts Focus From Record Demand to Fuel Costs

Carnival shares closed Tuesday at $28.72, down 4.87%, even after the cruise operator reported record second-quarter revenue, net yields and adjusted net income. Strong demand was not enough to keep costs from defining the earnings reaction.

Fuel cost per metric ton rose from $614 to $793, almost 29%, while constant-currency net yields increased 2.2%. Reuters reported that third-quarter profit guidance was below estimates as fuel costs rose. CCL now needs pricing and booking strength to defend margins, not merely keep ships full.

Bookings stayed full while gross margin yields fell

Revenue reached $6.663 billion, adjusted net income rose to $569 million and adjusted EBITDA reached $1.582 billion. Adjusted earnings improved, but the operating mix was less straightforward than the record labels suggest.

Carnival was 93% booked for 2026 and customer deposits reached $8.984 billion. Bookings for the rest of the year were ahead of the prior year at historically high prices, giving the company less unsold inventory and a clearer view of summer revenue.

Pricing still did not fully reach gross margin. Constant-currency net yields rose 2.2% and nonfuel cruise costs per berth day were flat, while gross margin yields fell 3.9%. Demand held; the cost of serving it changed.

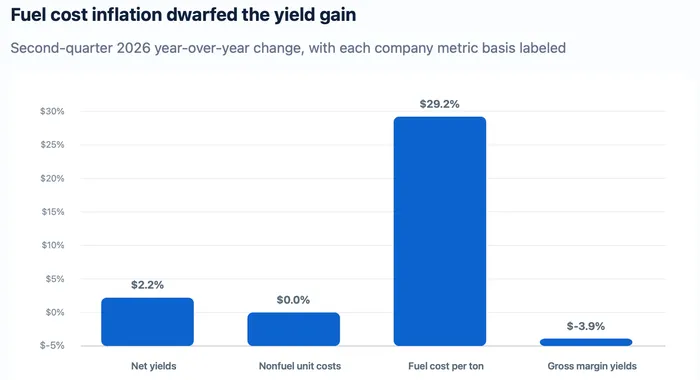

A 29% fuel shock outran the 2.2% yield gain

Fuel cost per metric ton increased to $793 from $614. That 29.2% rise was more than thirteen times the constant-currency net-yield gain and explains why a record revenue quarter could still produce weaker gross-margin yield.

Operational discipline softened the hit. Fuel consumption per berth day improved 5.6%, and nonfuel unit costs did not rise in constant currency. Efficiency reduced gallons consumed per unit of capacity, but it could not neutralize the price paid for fuel.

Fuel cost per metric ton rose 29.2%, while constant-currency net yields increased 2.2% and gross margin yields fell 3.9%.

Source Carnival earnings release filed June 23, 2026. Provider Carnival Corporation. Symbol CCL. Date range second-quarter 2026 versus prior year. Interval fiscal quarter. Basis constant-currency net yields and nonfuel unit costs, reported fuel cost per metric ton and reported gross margin yields. Fuel growth is calculated from $793 versus $614.

A reversal in fuel prices would help faster than another occupancy gain because the company already ran at 104% occupancy in both periods. Continued fuel inflation would do the opposite, turning a demand story into a cost and cash-flow problem.

Third-quarter guidance leaves little room for another cost spike

Carnival guided third-quarter adjusted EPS to about $1.35 and adjusted EBITDA to about $2.88 billion. The guide also assumes constant-currency net yields rise about 1.2%, less than the expected 2.8% increase in nonfuel unit costs.

Fuel adds another constraint. The company is using $812 per metric ton for the third quarter, above the second-quarter average. A 10% fuel-cost change would alter adjusted net income by $56 million, enough to matter against a guide that already missed market estimates.

European bookings are the counterweight. Management said demand for 2027 European deployments improved after March, and recent trends suggested Middle East-related pressure was beginning to reverse. Stronger pricing can recover some cost, but the third quarter must show that improvement in net yield and adjusted EBITDA.

Buybacks accelerate before leverage is fully repaired

Carnival generated $2.629 billion of operating cash and spent $875 million on capital expendituresduring the quarter. That leaves about $1.754 billion before dividends, repurchases and other financing uses, a useful measure of the cash available for competing priorities.

The company has repurchased more than $450 million of stock and paid $207 million of quarterly dividends. Debt still stood at $24.889 billion, down from $26.640 billion at the end of November, while net debt to adjusted EBITDA improved to 3.1 times.

Debt reduction is moving in the right direction, but fuel volatility can narrow operating cash after capex and slow that progress. More buybacks raise the return of cash to shareholders; a higher fuel bill raises the value of balance-sheet flexibility.

Third-quarter net yields near 1.2%, fuel near or below $812 per metric ton and adjusted EBITDA near $2.88 billion would show that pricing is covering the summer cost base. A stronger European booking recovery and leverage below 3.1 times would reinforce that outcome. Missing those markers would keep the June 23 decline tied to earnings quality rather than weak cruise demand.