onsemi's $7 Billion Synaptics Deal Made the Target Fall With the Buyer

onsemi acquires Synaptics for $7 billion, but a fixed stock ratio causes its shares to plummet 23 percent, tying target value to acquirer performance.

onsemi agreed on June 25 to acquire Synaptics in an all-stock transaction with an enterprise value of about $7 billion. The strategic pitch joins onsemi's power and sensing chips with Synaptics' edge compute, connectivity and human-machine interface products.

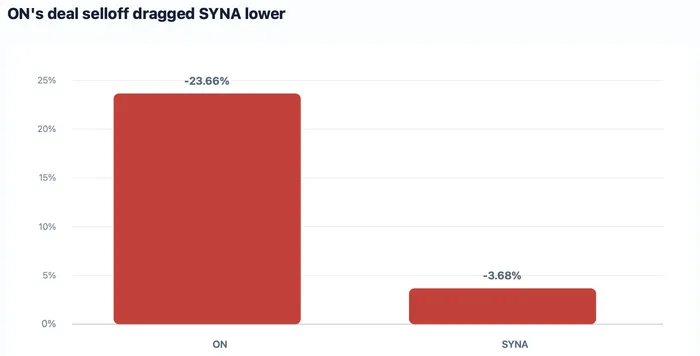

Friday's regular session delivered a harsher price verdict. ON closed at $90.65, down 23.66%, while SYNA finished at $121.00, down 3.68%. A fixed stock ratio made the target fall with the buyer, shifting attention from the Physical AI label to floating consideration, dilution and the timing of operating benefits.

Provider StockAnalysis ON and StockAnalysis SYNA using Nasdaq UTP market data. Symbols ON and SYNA. Date June 26, 2026. Interval regular session. Basis unadjusted close-to-close percentage change. Bars show decline magnitudes and labels retain minus signs.

The fixed ratio turned a premium into a moving target

A stock deal gives Synaptics no cash floor. Each SYNA share is due to convert into 1.350 ON shares, leaving Synaptics holders with about 12% of the combined company on a fully diluted basis.

Multiplying that ratio by ON's June 26 close gives $122.38 of implied consideration per SYNA share. SYNA's $121.00 close sat about 1.1% below that figure, a much narrower cushion than the announced 19% premium to the companies' 10-day volume-weighted average closing prices.

Such a structure explains why target holders could not escape the acquirer's selloff. The consideration can recover if ON rebounds, but it can also fall again before the vote and regulatory close. Deal-spread behavior now depends on ON's price as much as on approval odds.

onsemi is buying compute to complete its power stack

Strategy centers on filling a product gap. Synaptics adds connected compute, Wi-Fi, Bluetooth, GPS and human-machine interface products to onsemi's power and sensing base. The companies say the combination could add $30 billion of addressable market and reach $243 billion by 2030, figures that remain management estimates rather than booked revenue.

onsemi's latest operating base shows why the expansion is tempting. The company reported fiscal Q1 revenue of $1.513 billion, gross margin of 38.5% and non-GAAP operating margin of 19.1%. Power Solutions revenue rose 14% year over year, while Analog and Mixed-Signal fell 5% and Intelligent Sensing rose 1%.

Management wants a broader system sale that can raise semiconductor content per automotive, industrial or robotics platform. Customer adoption is the missing bridge. A larger product catalog creates value only if common software, sales coverage and product roadmaps turn separate chips into more revenue per design.

Synaptics adds margin, along with a mixed end-market cycle

Synaptics brings a different margin and growth profile. It reported fiscal Q3 revenue of $294.2 million, Core IoT product-sales growth of 31% and non-GAAP gross margin of 53.6%. Those figures support the case that connected compute and IoT can improve the combined mix.

Consumer and wireless exposure adds a less uniform cycle. Core IoT units rose 27.1% and average selling prices rose 2.9%, while Mobile units fell 5.7% and average selling prices fell 11.2% in the March quarter. The acquisition therefore mixes a strong IoT pocket with applications still facing volume and pricing pressure.

Cost savings could soften that risk. onsemi expects $200 million of annual synergies and non-GAAP EPS accretion within 18 months after closing. Both remain forecasts. Preserving Synaptics' margin while integrating products and sales teams will matter more than the headline addressable market.

The S-4 now has to carry the strategy

Closing is expected in mid-2027 and still requires Synaptics stockholder approval, regulatory clearances and other conditions. The merger agreement includes a $235 million Synaptics termination fee and a $320 million onsemi regulatory termination fee under specified circumstances.

The next filing should make three items easier to judge. Pro forma financials can show the true margin mix, the synergy bridge can separate cost savings from hoped-for revenue gains, and the ownership table can quantify dilution against current share counts. Quarterly results must then show whether Core IoT strength survives while Mobile pricing stabilizes.

Friday's selloff did not settle the strategic case. It raised the operating bar. A durable recovery would require the combined company to preserve Synaptics' margin mix, convert the stated savings and show that edge-compute products expand onsemi's automotive and industrial content. Without those disclosures, the fixed ratio keeps both stocks tied to an integration plan whose benefits arrive later than the shares.