General Mills Jumped 8.5% After Earnings Beat, but Volumes Still Fell

General Mills shares surged 8.5% after beating profit estimates, though organic sales remained flat as higher prices masked a two percent decline in consumer volume.

General Mills shares closed 8.5% higher on Wednesday after the Cheerios maker beat quarterly profit estimates and announced a four-year savings program. Adjusted earnings of $0.95 a share topped the $0.80 average estimate compiled by LSEG.

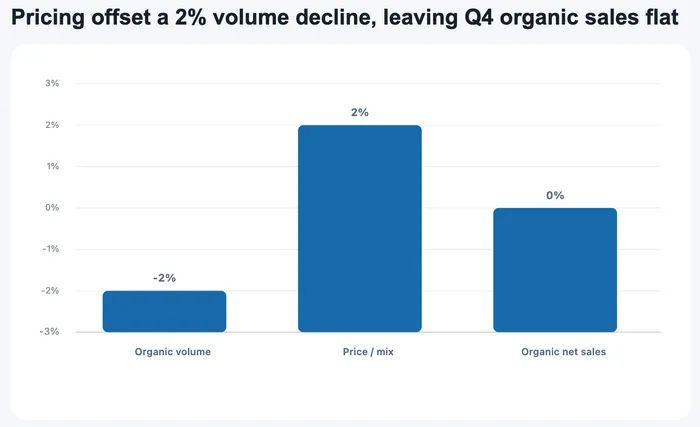

The rally changed the immediate debate around GIS, which Reuters said had fallen 25% in 2026 before the report. It points to relief that profit can stabilize before demand fully recovers. General Mills' own sales bridge shows why that distinction matters. Organic volume fell 2%, while price and mix rose 2%, leaving organic sales flat.

The earnings relief arrived before demand recovered

Fiscal fourth-quarter net sales rose, but the reported number included an extra week and portfolio changes that make the headline a poor measure of underlying demand. On the underlying organic basis, sales were unchanged. Adjusted operating profit increased, helped by higher gross profit and favorable trade-expense timing.

Those details make the stock move easier to interpret. A business can deliver an earnings surprise while units remain soft when pricing, mix and cost control carry more of the burden. GIS is the direct packaged-food exposure to that equation because volume, pricing and savings all sit inside the same issuer. That is a better result than continued profit erosion, but it does not establish that households are buying more General Mills products.

Non-cash impairments and a valuation loss also pushed reported operating results deeply negative, so the quarter is best read through the company's adjusted figures. The risk is that temporary timing benefits fade before volume improves. Fiscal 2027's opening quarter will need to show whether North America Retail can hold sales and profit without another unusual bridge.

Pricing offset a 2% volume decline, leaving organic sales flat

Company data separate the two forces behind the quarter. Lower volume removed two percentage points from organic sales, while price and mix added two. Flat organic sales therefore reflected offsetting pressures, not a broad demand recovery.

Price realization can protect gross profit when shoppers accept higher prices or shift toward richer products. Persistent volume weakness works the other way because fewer units leave a smaller revenue base for fixed costs, marketing and product investment. Promotions may rebuild traffic, but they can also give back part of the margin benefit.

Source General Mills. Symbols GIS. Date range fiscal Q4 2026. Interval fiscal quarter. Basis is the company-reported organic net-sales contribution. General Mills results.

The $3 billion savings plan is an earnings bridge, not a sales catalyst

General Mills plans to generate $3 billion in cumulative savings through fiscal 2030, with at least $750 million expected in fiscal 2027. Roughly two-thirds of the long-range target is tied to its productivity program; the rest is expected from supply-chain redesign, streamlined processes and other efficiency work.

That program matters because management intends to offset input-cost inflation while funding product renovation and marketing. It can improve the profit equation even if categories grow slowly. It cannot create consumer demand by itself, and every dollar reinvested in brands delays how much of the savings reaches operating profit.

Execution therefore matters more than the headline total. Reported savings, adjusted operating margin and free cash flow will show whether efficiency is outrunning inflation and reinvestment, or merely preventing a larger decline.

Fiscal 2027 guidance keeps the rally conditional

The company's outlook leaves room for another difficult year. Fiscal 2027 organic sales are expected to range from down 1.5% to up 0.5%, while adjusted operating profit is projected to decline in constant currency.

Management attributes part of the pressure to lapping the extra week, portfolio changes and normalized compensation, not just weaker demand. That comparability matters, but it does not remove the operating burden. Price investment and new products still have to lift volume enough for savings to produce durable earnings growth.

The next useful read will come from North America Retail volume, organic sales and adjusted operating profit, alongside the pace of the $750 million fiscal 2027 savings target. If those measures improve together, the July 1 rally will look like the start of a recovery. If profit holds only because pricing offsets fewer units, GIS remains a cost-control story with demand still unresolved.