Meta Just Flipped The AI Hardware Trade: Why Memory Stocks Crashed?

Meta did not announce a new chip. It changed the market’s question. If one of the world’s biggest AI spenders can sell excess compute to outside customers, investors must now ask whether the AI hardware boom is still a pure scarcity story, or whether the next phase is about utilization, pricing pressure and shareholder returns.

Meta Rallied Because The Market Saw A New Return On AI Spending

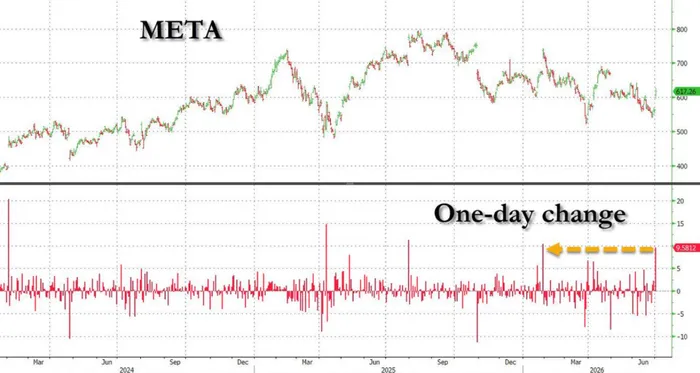

The sharpest move in the AI trade this week did not come from Nvidia, Micron or a Korean memory supplier. It came from Meta.

Meta shares jumped nearly 9% after Bloomberg reports is building a cloud-style business to sell excess AI compute to outside customers. The project, reportedly organized under a new “Meta Compute” structure, would allow Meta to monetize part of the massive AI infrastructure it has been building for internal model training, inference and product development.

That is why the stock rallied while many AI hardware names sold off. For months, investors worried that Meta’s AI capex was becoming an open-ended cost center. The new narrative is different: if Meta can resell unused compute, capex becomes less of a burden and more like an asset that can generate revenue.

This is an important shift. The market is no longer simply rewarding the company that spends the most on AI infrastructure. It is starting to reward the company that can prove AI spending has a path to returns.

Memory Stocks Fell Because Scarcity Was The Whole Trade

That same logic hurt memory and semiconductor stocks.

Micron fell more than 10%, SanDisk also dropped sharply, and the Philadelphia Semiconductor Index lost over 6%. The selloff was not just about one company’s plan. It hit the core assumption behind the memory-chip rally: AI compute is scarce, memory is scarce, hyperscalers will keep buying aggressively, and suppliers will keep enjoying pricing power.

Meta’s plan challenges that story at the margin. If a hyperscaler has enough excess AI capacity to sell externally, then the market has to consider a more uncomfortable possibility: some AI infrastructure may be overbuilt, underutilized or at least more price-sensitive than bulls assumed.

That does not mean AI demand is collapsing. It does mean the “absolute scarcity” premium is less bulletproof. Once investors start asking whether compute can be resold, rented, optimized or repriced, they also start questioning how long memory suppliers can keep charging peak-cycle prices.

This is why the reaction was so violent. Memory stocks had already priced in a powerful cycle, helped by tight HBM supply, strong DRAM pricing and the belief that AI capex would keep expanding almost regardless of cost. In that setup, even a small crack in the demand narrative can trigger a large positioning unwind.

The Bigger Risk Is Not Today’s Demand, But Tomorrow’s Buyer Behavior

The near-term memory market still looks tight. AI servers need enormous amounts of HBM and DRAM, and supply cannot be added overnight. On that basis, the bull case has not disappeared.

But the risk has changed.

The first risk is cloud capex discipline. If Meta is the first major hyperscaler to openly frame AI infrastructure around utilization and monetization, investors will watch whether Microsoft, Amazon, Alphabet and others follow with similar language during Q2 earnings. Any sign that capex growth is slowing, being front-loaded or being managed more tightly could pressure the entire AI hardware chain.

The second risk is innovation. As the WSJ noted, the long-term threat to the memory boom may not be weak demand, but customer adaptation. When chips are expensive or scarce, large buyers look for ways to use less memory per unit of output, redesign systems, optimize software, or shift workloads. That kind of innovation does not break a cycle overnight, but it can cap the upside over time.

The third risk is alternative sourcing. Bloomberg reported that Apple is seeking to buy Chinese-made memory chips through a lobbying push. If large buyers can bring more suppliers into the chain, even gradually, it weakens the assumption that incumbent memory leaders will face no pricing resistance.

The fourth risk is compute pricing itself. If GPU rental prices or AI compute spot prices soften, investors will read that as evidence that the scarcity premium is fading. That makes SemiAnalysis’ GPU Pricing Index worth watching closely. A falling compute-price curve would be a direct warning signal for the hardware trade.

Q2 Earnings Will Decide Whether This Is A Shakeout Or A Bigger Reset

The next major test is Q2 earnings from the cloud giants.

The key question is not whether AI demand is still growing. It almost certainly is. The question is whether AI infrastructure spending keeps accelerating at the same pace.

Investors should watch for a few phrases: “higher utilization,” “capex discipline,” “front-loaded investment,” “external compute sales,” “capacity optimization,” and “more efficient AI infrastructure.” If these words show up repeatedly across hyperscaler calls, the market may start treating the memory rally as a late-cycle trade rather than an early-cycle shortage story.

The bullish version is simple: Meta’s move is a smart monetization strategy, not a demand warning. AI workloads keep growing, memory supply remains tight, and the selloff becomes a buying opportunity after an overheated run.

The bearish version is more dangerous: Meta is the first sign that AI infrastructure is moving from panic buying to cost control. If that is right, memory stocks may still have strong earnings in the near term, but valuation multiples could compress as investors stop paying peak prices for a peak-scarcity story.

For now, the trade has changed. The market is no longer asking only who can supply the AI boom. It is asking who can still profit if the AI boom becomes more efficient.