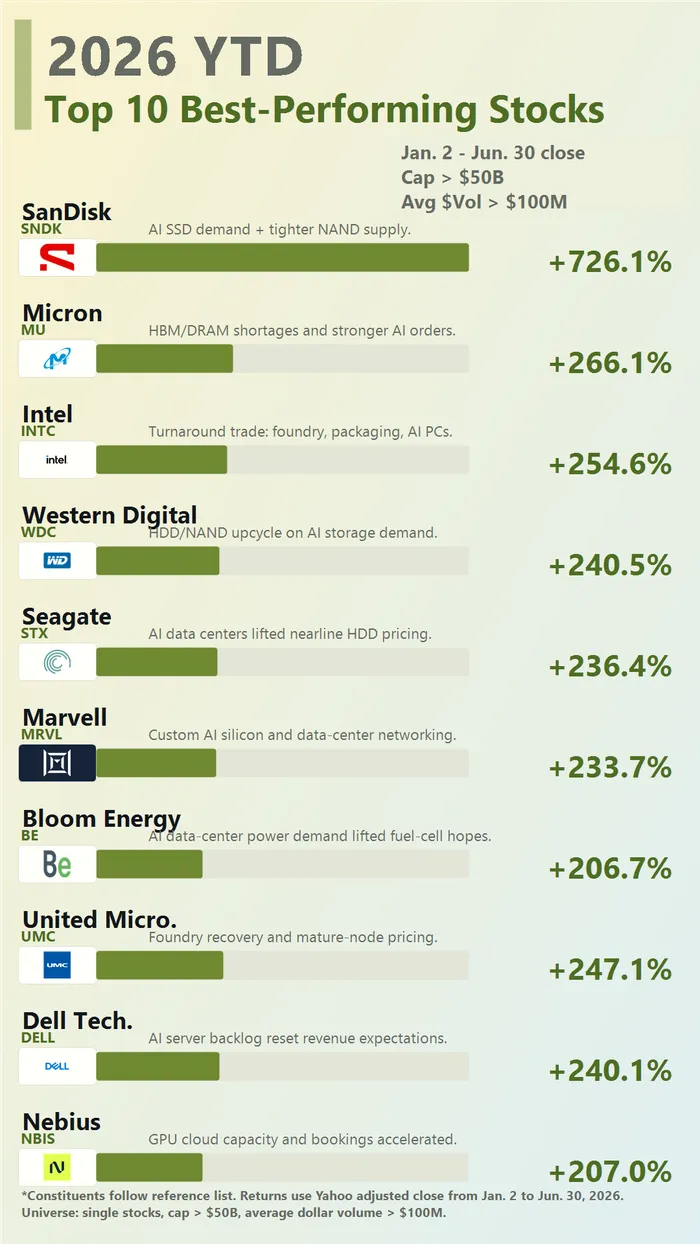

10 Best & Worst Stocks in H1 2026: AI Infrastructure Won, Software Got Repriced

AI infrastructure stocks surged on scarcity while software firms faced repricing as investors demand proof that AI agents enhance rather than replace existing revenue models.

The first half of 2026 did not produce a broad “AI rally.” It produced a much narrower and more tradable split: companies tied to AI infrastructure, memory, storage, servers and power were aggressively re-rated, while software and service companies were punished for the risk that AI agents could compress their pricing power.

The top performers were almost a supply-chain map of the AI buildout. SanDisk, Micron, Western Digital and Seagate captured the storage and memory cycle. Marvell sat in custom AI silicon, optics and data-center networking. Dell was a server backlog story. Nebius was a GPU-cloud capacity story. Intel traded as a turnaround option on foundry, advanced packaging and AI PCs. Bloom Energy added a different but related angle: power demand from AI data centers.

The common feature was not “AI exposure” in a loose marketing sense. It was bottleneck exposure. These companies were tied to parts of the stack where demand was visible, supply was constrained, pricing was moving in the right direction, or earnings estimates could be revised higher quickly.

That is why the rally looked so concentrated. The market was not simply buying growth. It was buying scarcity.

Memory Became The Cleanest AI Trade

The strongest cluster was memory and storage. Micron, SanDisk, Western Digital and Seagate benefited from the same core argument: AI data centers require more than GPUs. They require high-bandwidth memory, DRAM, NAND, SSDs, hard drives and fast data movement. When AI capex stays strong, the storage layer becomes a direct beneficiary.

Wall Street’s second-half debate is therefore not whether AI matters. It is whether the memory and storage cycle has already discounted too much good news. Bulls argue that supply relief takes time, pricing power is visible and hyperscaler capex remains resilient. Bears argue that the stocks have already pulled forward a large amount of earnings recovery and would be vulnerable if cloud capex slows.

The trading implication is simple: memory winners can keep working only if contract pricing, backlog and gross-margin guidance continue to confirm the shortage thesis.

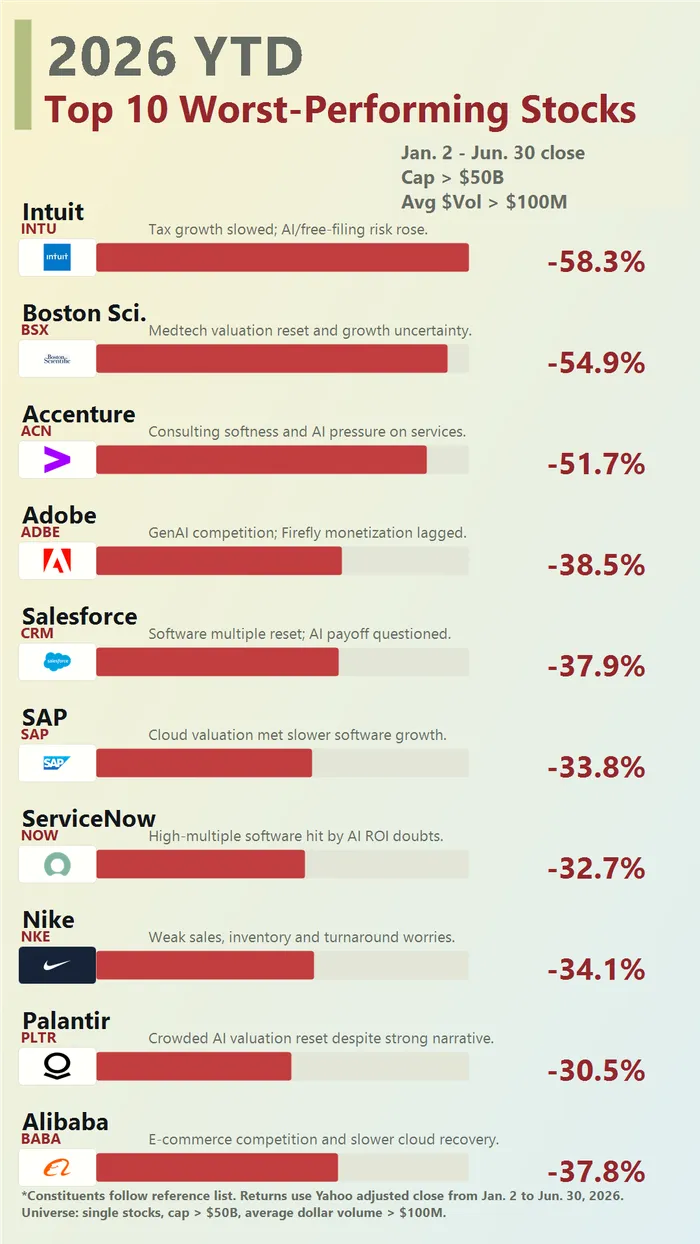

Software Was Repriced Around AI Disruption

The losers told the other half of the story. Intuit, Accenture, Adobe, Salesforce, SAP, ServiceNow and Palantir were all caught in a software valuation reset. The market is no longer treating recurring revenue as an automatic moat. It is asking whether AI agents will enhance these platforms or bypass parts of their workflow.

This does not mean all software is broken. It means investors now demand evidence. Can AI features lift average revenue per user? Can vendors charge for agentic workflows? Will AI raise retention, or will it compress seat counts and implementation work? Can gross margins hold if inference costs rise?

That is why the selloff was not just about one bad quarter. It was a change in the questions investors ask about software.

Not Every Loser Was An AI Story

Nike was the clearest non-AI outlier. Its weakness was more traditional: soft sales, inventory pressure, brand reset risk and uncertainty around the turnaround. The stock’s path depends less on AI and more on product heat, China demand, wholesale recovery and margin repair.

Alibaba also belongs in a different bucket from U.S. enterprise software. Its pressure came from e-commerce competition, slower cloud recovery and macro/regulatory uncertainty around China assets. It can rebound, but the trigger is more likely to be a combination of consumer stabilization, cloud acceleration and reduced competitive pressure than a simple AI narrative.

Bloom Energy is the mirror image on the winner side. It is not a chip stock. Its inclusion shows that the AI trade has spread into power infrastructure. If data-center electricity demand stays tight, power and grid-adjacent names can remain part of the AI basket.

H2 Outlook: Still Bullish On AI Infrastructure, But Less Forgiving

Major second-half outlooks from financial media and strategists generally do not call the AI trade over. MarketWatch cited the possibility that the AI trade could still power the market higher. Business Insider reported Goldman Sachs’ view that investors should keep leaning into AI infrastructure, AI power infrastructure and hyperscalers. Fidelity’s AI outlook also frames AI as a multi-year infrastructure cycle rather than a short software theme.

But the second half should be less forgiving than the first. The easiest re-rating has already happened in many memory and storage names. From here, the market will likely demand earnings delivery: better pricing, stronger backlog, sustained capex and visible margin expansion.

The key risk is capex fatigue. If hyperscalers slow data-center spending, the same stocks that benefited most from AI infrastructure could correct fastest. The other risk is valuation compression: even a good cycle can become a bad trade if expectations move too far ahead of profits.

Can The Losers Reverse?

Yes, but the setup differs by group.

Software can rebound fastest if the market decides the AI disruption fear has gone too far. Adobe, Salesforce, SAP, ServiceNow, Intuit and Palantir do not need investors to forget AI risk. They need to prove AI is revenue-accretive rather than seat-destructive. The next confirmation points are AI product adoption, pricing, retention, billings and margin guidance.

Nike is a slower turnaround. It needs better sales momentum, inventory cleanup and brand execution. A single relief rally is possible, but a durable rerating requires operating proof.

Alibaba needs a different catalyst set: better China consumption data, less aggressive e-commerce competition, cloud growth recovery and a more supportive policy or capital-market backdrop.

The final H2 takeaway is not “buy winners and avoid losers.” It is more precise: own AI infrastructure only where earnings still have room to move up, and buy beaten-down software only where management can show AI is a monetization layer rather than a substitute.