June Nonfarm Payrolls Well Below Expectations, but Lower Unemployment Complicates Fed Hike Bets

June payrolls missed forecasts sharply, yet steady wage growth and low unemployment complicate bets on a Federal Reserve rate pause.

U.S. job growth slowed sharply in June, adding fresh evidence that the labor market is cooling as investors debate whether the Federal Reserve will move forward with another rate hike later this year.

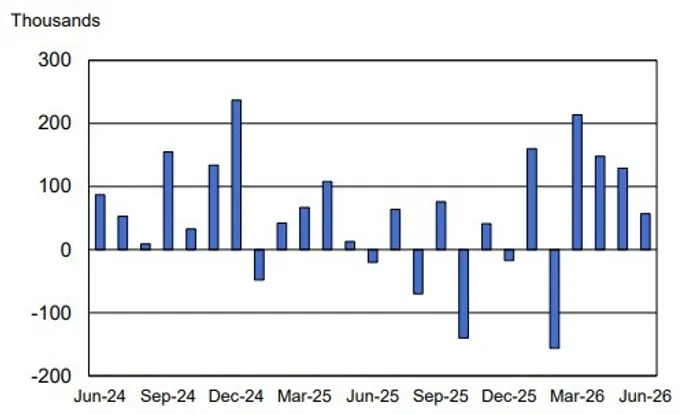

Nonfarm payrolls increased by 57,000 in June, according to the Bureau of Labor Statistics, well below the Dow Jones consensus forecast of 115,000. The gain also marked a sharp slowdown from May, which was revised down to 129,000 from the previously reported 172,000. April payrolls were also revised lower, from 179,000 to 148,000. Together, April and May employment gains were revised down by 74,000.

Despite the weak headline payroll number, the unemployment rate fell to 4.2%, slightly below expectations. However, the decline was largely driven by a drop in labor force participation, which fell 0.3 percentage point to 61.5%. The employment-population ratio also edged down to 59.0%, suggesting the lower unemployment rate was not entirely a sign of stronger labor demand.

The details of the report showed an uneven job market. Employment continued to trend higher in professional and business services, social assistance, and health care, while leisure and hospitality posted a notable decline. Professional and business services added 36,000 jobs in June, social assistance gained 25,000, and health care rose by 22,000. Leisure and hospitality lost 61,000 jobs, reflecting weaker-than-usual seasonal hiring and extending a sluggish trend for the sector so far this year.

Wage growth remained steady, keeping the inflation debate alive. Average hourly earnings rose 0.3% in June to $37.64, while year-over-year wage growth held at 3.5%. The average workweek for all private-sector employees was unchanged at 34.3 hours, while the workweek for production and nonsupervisory employees slipped by 0.1 hour to 33.7 hours.

The report presents a mixed picture for the Fed. On one hand, the sharp payroll miss and downward revisions suggest labor demand is losing momentum. The rise in long-term unemployment also points to more difficulty for job seekers, with 1.9 million Americans unemployed for 27 weeks or longer, up 286,000 from a year earlier.

On the other hand, the unemployment rate remains relatively low, wage growth is still firm, and several service categories continue to add jobs. That combination may prevent the Fed from treating the June report as a clear signal that the economy is weakening fast enough to delay policy tightening.

The data comes shortly after new Fed Chair Kevin Warsh said the inflation outlook had improved since the central bank's previous meeting, while emphasizing that price pressures remain too elevated. Warsh also declined to provide direct rate guidance, reinforcing that the Fed's next move will depend heavily on incoming economic data.

Markets are now likely to focus on whether the softer payroll trend is enough to push back expectations for another rate hike. According to FedWatch, markets still see more than a 65% chance of a rate increase by the September meeting. The June jobs report could challenge that view, but it may not be enough by itself to remove the risk of further tightening.

That makes the next inflation report, due on July 14, even more important. If price data continues to moderate, the June payroll miss could strengthen the case for delaying the next hike. But if inflation remains sticky, the Fed may still view the labor market as strong enough to tolerate another move higher in rates.