Liquidity Continues Supporting the Bull Market as Rotation Replaces Panic and Volatility Normalizes

The stock market is entering the second half of 2026 with more challenges ahead, as AI competition heats up, investors question the sustainability of aggressive capital spending, Fed rate-hike risk remains alive, and major events such as the Anthropic IPO could further reshape sentiment. Still, the broader market remains solid, with the S&P 500 hovering near highs even as the tech-heavy Nasdaq pulls back. Concerns also grew that Meta's cloud expansion could be a warning sign of future computing oversupply. At the same time, weak job data reduced expectations for another near-term rate hike and pushed the dollar lower, although Fed tightening is not fully off the table. The latest rotation suggests that speculative momentum in technology is cooling, but capital is not leaving the broader market. More importantly, longer-term liquidity conditions continue to provide support, even as short-term technical risks and elevated yields remain important.

Weak employment data reduced expectations for another near-term rate hike and pushed the dollar lower, but Fed tightening is still not fully off the table. The latest rotation suggests that speculative momentum in technology is cooling, but capital is not leaving the broader market. More importantly, longer-term liquidity conditions continue to provide support, even as short-term technical risks and elevated yields remain important.

From a technical perspective, the S&P 500 remains within a broader higher-low structure and continues to trade near the key 7,500 resistance area. This level has become increasingly important because the index has struggled to extend above it, creating some ambiguity around a potential triple-top pattern. A decisive breakout to a new high would be needed to fully verify the next bullish leg, while failure to clear this zone could keep the market trapped in consolidation.

The key may still come from chip stocks, given their heavy weight in both the index and market psychology. Semiconductor weakness has become the most important short-term drag, and investors need to see whether AI demand can outweigh oversupply concerns. Meta's cloud push may also suggest that fewer AI players will dominate the long-term infrastructure race, raising questions about whether every company can justify continued aggressive expansion. For the S&P 500, the most important support remains near 7,300. A decisive break below that level could open the door to another move toward 7,200 and potentially the psychological 7,000 area.

Volume dynamics also reflect a market moving from aggressive speculation toward more selective positioning. Trading conditions were thinner ahead of the Independence Day holiday, while the strongest activity remained concentrated in former AI leaders as investors locked in gains. The Philadelphia Semiconductor Index fell almost 7%, yet the broader S&P 500 remained relatively stable. This indicates that the selling was driven more by profit taking in crowded positions than by broad institutional liquidation.

Market breadth provides a more constructive signal beneath the surface. More than two-thirds of S&P 500 stocks advanced on Thursday even as the Nasdaq declined, while the advance-decline line continued to trend higher. This suggests that broad support remains in place, with semiconductors serving as the main area of pressure. The divergence helps reduce concentration risk, as the market is beginning to rotate away from the most crowded AI trade without damaging the broader index.

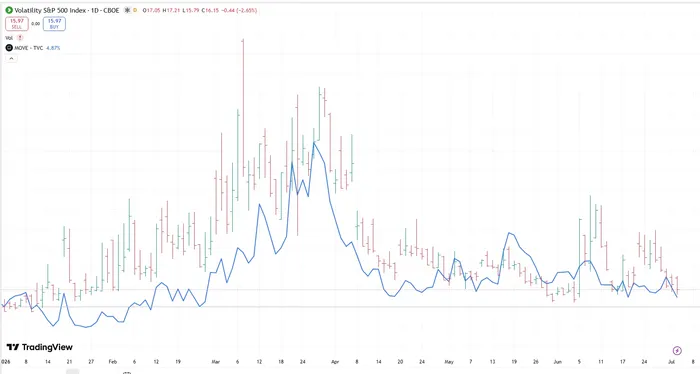

Volatility indicators further support the view that the recent weakness is an orderly rotation rather than the beginning of systemic stress. The VIX fell toward 16 despite the sharp decline in chip stocks, showing that demand for broad equity protection remains limited. The MOVE index, which measures volatility in the Treasury market, was near 65, its lowest level since April, as weak nonfarm payrolls helped ease concerns about an immediate Fed hike. Neither indicator is signaling disorderly hedging, which is important because a genuine liquidity event would normally produce simultaneous pressure across both equity and bond volatility.

Longer-term liquidity remains the most important support for the market. Overall liquidity has been trending higher since November, when the Fed stopped shrinking its balance sheet. The Fed's balance sheet has moderated only slightly to around $6.7 trillion for the week ending July 1, while the Treasury General Account also moved slightly lower to around $807 billion, without a material change in direction. This liquidity backdrop continues to provide broad support, but the next key question will be how new Fed Chair Kevin Warsh manages the balance sheet.

Still, investors should not worry too much, at least for now. After the weak jobs data, the dollar index fell toward 101 as expectations for a near-term hike declined. The 2-year Treasury yield stood near 4.14%, while the 10-year yield was near 4.48%. The 10-year minus 2-year spread has widened, leaving the yield curve more normalized. The bond market is therefore becoming more balanced, although not yet fully supportive.

The next inflation report will be critical because it could determine whether the Fed still has enough justification to hike again. From our perspective, Warsh is unlikely to favor an extended hiking cycle. Even if another hike happens, it may be short-lived, possibly limited to one or two moves, rather than the start of a sustained tightening campaign. As oil-fueled inflation slows, inflation is unlikely to become the same kind of market-breaking problem that investors faced in 2022.

Meanwhile, gold and Bitcoin both strengthened after the employment report as the dollar weakened and rate-hike expectations eased. Gold moved toward $4,220, while Bitcoin recovered above $61,000. Their simultaneous advance suggests that investors are responding to lower policy pressure rather than simply moving into defensive assets. However, Bitcoin still faces more challenges because demand remains fragile, while gold continues to benefit more directly from a weaker dollar and lower expected rates.

Therefore, the latest signals suggest that the market is moving through a healthy but incomplete rotation. Semiconductor selling remains intense, and elevated real yields continue to create valuation pressure. At the same time, broader participation has improved, volatility remains contained, the yield curve is positively sloped, and the Fed has moved away from sustained balance-sheet contraction. From a trading perspective, the market still favors a selective buy-the-dip strategy rather than aggressive chasing. As long as the S&P 500 holds above 7,300 and volatility remains contained, pullbacks in strong non-chip sectors may continue to offer opportunities. The biggest warning sign would be a break below 7,300 combined with rising VIX, rising MOVE, and renewed dollar strength. For now, liquidity still supports the bull market, but the next upside leg needs stronger confirmation.