OPEC+ Raises August Quotas by 188,000 Barrels a Day as Brent Slips 0.3%

OPEC+ raises August quotas by 188,000 barrels daily, yet Brent crude slips 0.3% as markets price in the expected supply increase.

Seven OPEC+ countries raised August production quotas by 188,000 barrels per day on July 5. Oil barely reacted when trading resumed. Brent slipped 0.33% to $71.88 and WTI fell 0.16% to $68.58 at 0010 GMT on Monday.

The muted move changes the useful question. Brent's role as the global seaborne benchmark makes its small reaction especially useful, while WTI carries the same shock through a U.S. delivery basis. Another quota increase is bearish only if producers can lift output, move crude through export routes and find buyers. Reuters said the decision was largely expected, while earlier increases had remained partly on paper. Physical supply and demand now carry more weight than the headline target.

A 0.3% Brent move says the quota increase was expected

OPEC+'s decision extended the same 188,000-barrel monthly pace used for June and July. An IG analyst told Reuters the figure was largely in line with expectations. Futures therefore had little new information to absorb when Asian trading began.

Early price action has limits. A 0010 GMT quote is not a daily settlement, and U.S. markets had been closed ahead of the Independence Day holiday. Still, the small opening decline suggests the meeting confirmed an existing supply path rather than delivering a surprise. Monday's full session can strengthen or weaken that reading.

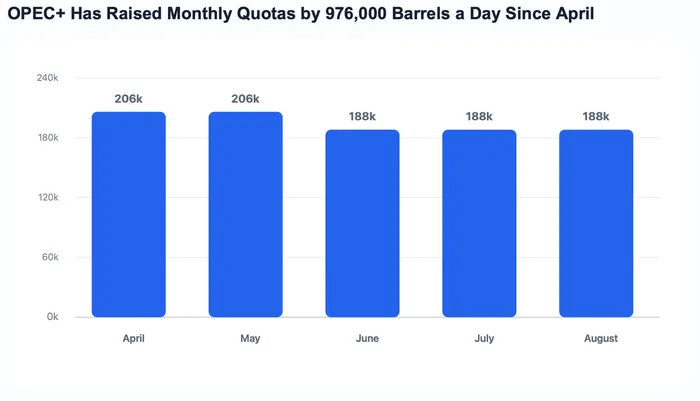

Five monthly quota increases add up to 976,000 barrels a day

Monthly quota additions began at 206,000 barrels per day for April and May, then slowed to 188,000 for June, July and August. The five decisions add up to 976,000 barrels per day of higher required production levels. Each figure is a policy ceiling, not evidence that the same volume reached buyers.

Sources and provider are official OPEC+ production-adjustment statements. The assets are OPEC+ crude quotas, not traded symbols. The date range covers April through August 2026. The interval is monthly. The basis is thousand barrels per day added to required production levels; these are quota changes, not measured output. The series is stitched from five official decisions and needs no price adjustment. April decision, May decision, June decision, July decision and August decision.

The pattern shows a managed rollback rather than an open-ended production surge. OPEC+ retained the flexibility to increase, pause or reverse the phase-out as market conditions change. Reuters calculated that roughly 379,000 barrels per day of the original 2023 cut would still remain after August, leaving another policy decision for September.

Exports, not targets, determine how much supply reaches buyers

Physical flows are recovering faster than the small price move implies. Reuters estimated OPEC output rose 3.3 million barrels per day in June to 19.43 million. Gulf exports exceeded 10 million barrels per day, but they remained 40% below prewar levels. The gap explains why a higher quota can coexist with constrained delivered supply.

Shipping capacity, field restarts and compensation for earlier overproduction all affect the conversion from targets to exports. If Gulf tanker flows normalize quickly while demand stays weak, additional barrels can pressure inventories and prices. Renewed disruption or slower restarts would keep the official quota above what the market can actually receive.

Demand and the August 2 review now carry the larger price risk

Demand is the other side of the balance. Reuters linked oil's return toward prewar levels to weaker Chinese imports, higher non-Middle East exports and a record coordinated strategic stock release. Those forces can outweigh a single 188,000-barrel quota step because they change how much crude the market needs and how much alternative supply is available.

The next U.S. Weekly Petroleum Status Report is scheduled for July 8. Inventories and imports will offer a near-term demand and balance check. OPEC+ will meet again on August 2, when July production, country compliance and export recovery can inform the September decision. Falling stocks or stronger Chinese buying would soften the surplus case; rising inventories alongside normalized exports would make the quota path more consequential.