BofA Says Korea’s $517B Memory Plan Won’t Kill The Supercycle, But Morgan Stanley Warns Against Going All In On Semis

One headline says Korea is spending hundreds of billions on new memory fabs. Another says investors are still lining up for SK Hynix. The trading message is more nuanced: the memory supercycle is not dead, but after a historic semiconductor rally, the next leg of the AI trade may not belong only to chipmakers.

South Korea’s planned 800 trillion won($517 billion), memory-chip cluster has triggered a familiar fear: if governments and chipmakers are spending this much on capacity, the cycle must be near the top.

That may be the wrong conclusion.

BofA analyst Simon Woo argues the new cluster is too far away to change the near-term supply picture. The project is not expected to produce meaningful chip output before 2033, and it comes after the existing Yongin and Pyeongtaek expansion cycle, which is planned across 2026 to 2035. In other words, this is a long-term industrial policy story, not an immediate supply shock.

That matters because the current memory market is still being driven by tight AI-related supply, not by future press releases. HBM, enterprise SSDs and advanced DRAM remain constrained by equipment lead times, packaging bottlenecks and qualification cycles. New fabs do not solve those problems quickly.

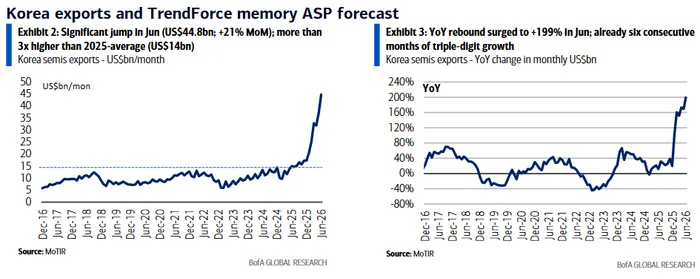

The data still points to a strong upcycle. South Korea’s June semiconductor exports rose to $44.8 billion, up 21% month over month and 199% year over year, marking a sixth straight month of triple-digit annual growth.

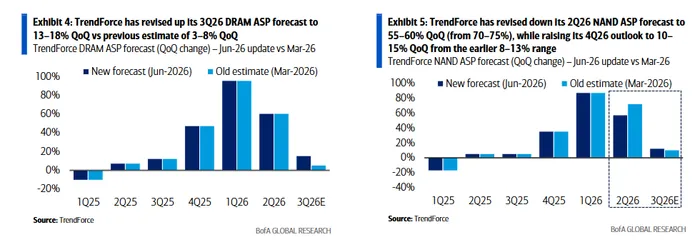

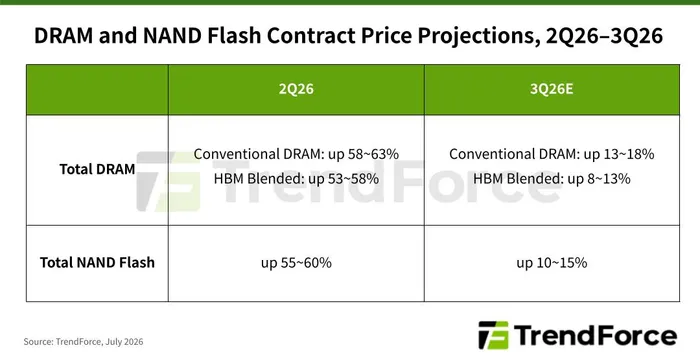

TrendForce also raised its third-quarter DRAM average price forecast to a 13% to 18% increase, from its prior 3% to 8% estimate.

Spot and contract pricing tell the same story. DRAMeXchange data cited in the reports showed 16Gb DDR5 spot prices near record highs, while NAND pricing has also recovered sharply from last year’s lows. This is not what a supply-glut market looks like.

Hynix Demand Shows Investors Still Want The Cycle

The strongest counterargument to “memory cycle top” is investor demand for SK Hynix itself.

SK Hynix has launched bookbuilding for a US listing that could raise about 43.1 trillion won, or roughly $28 billion, after an earlier reference value near 45.5 trillion won, or about $29 billion. The adjustment was driven by recent share-price movement, not by a collapse in demand.

The deal has already drawn about $7 billion of indicated investor interest, roughly a quarter of the expected offering size. That is a meaningful signal: even after a huge rally in memory stocks, global capital still wants access to the leading HBM supplier.

The reason is straightforward. SK Hynix remains one of the clearest equity proxies for AI memory demand. Counterpoint data cited in the reports showed the company held 57% of global HBM revenue share in the fourth quarter of 2025. Its first-quarter operating profit also jumped to a record, supported by AI data-center demand and pricing power.

But The Trade Is No Longer “Buy Every Chip Stock”

The more important shift may be in market leadership.

Morgan Stanley’s Michael Wilson says semiconductor momentum is fading. The Philadelphia Semiconductor Index has fallen nearly 14% from last month’s high, even though it remains up more than 120% since last September. That is exactly the kind of setup where good news starts to matter less and positioning starts to matter more.

Wilson’s message is not that AI is over. It is that investors should not be all in on semiconductors after such a powerful run. He now prefers AI hyperscalers such as Microsoft, Amazon and Meta, arguing that these companies have strong core businesses and may become the next place for capital to rotate.

That view fits the new phase of the AI trade. In the first phase, investors wanted the scarce hardware: GPUs, HBM, advanced packaging and memory. In the next phase, they may reward the companies that can turn massive AI spending into revenue, margins and shareholder returns.

This is why the Magnificent Seven platforms matter again. Microsoft, Amazon, Alphabet and Meta are still the buyers funding the AI infrastructure cycle. BofA expects combined 2026 capex from those four hyperscalers to rise about 80% to roughly $700 billion, with 2027-2028 spending potentially approaching $1 trillion. If that spending holds, the memory trade still has support.

But if the same companies start talking more about capex discipline, utilization and returns, the equity market may prefer the platforms over the suppliers.