Trump's Iran Ceasefire Extension Isn't a Buy Signal for Airline Stocks

Trump's late-Tuesday decision to extend the U.S.-Iran ceasefire indefinitely looked, at first glance, like the kind of headline that should lift airlines and other fuel-sensitive stocks. The problem is that Tehran has not agreed to a broader deal, the U.S. naval blockade remains in place, and the Strait of Hormuz is still functioning like a bottleneck rather than an open artery. For investors, that means the obvious relief-trade explanation is incomplete: the real market variable is physical oil flow, not the ceasefire wording.

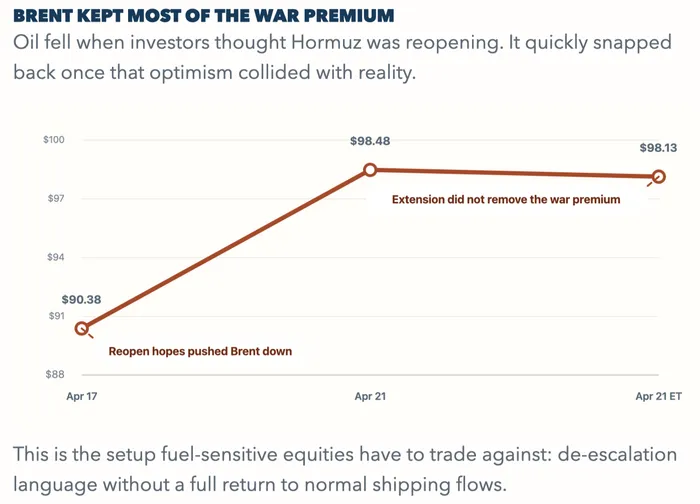

Markets reflected that gap fast. On April 21, the S&P 500 fell 0.6% as peace talks stumbled, while Brent crude settled at $98.48 a barrel after swinging from below $95 to roughly $100 during the session. Even after Trump said on April 21 that the ceasefire would be extended, WTI still traded near $90.26 early on April 22 because talks remained uncertain and Hormuz was still effectively closed. Only three vessels passed through Hormuz in the prior 24 hours, which is nowhere near normal traffic and helps explain why the ceasefire headline did not fully remove the war premium from crude. That matters directly for carriers: Delta said June-quarter jet fuel could average about $4.30 a gallon, a reminder that airline margin pressure does not disappear just because the diplomatic language sounds calmer.

Source: AP on April 17, AP on April 21, and Reuters on April 22. The chart is a three-point snapshot, not a continuous intraday series.

WHY THE FIRST RELIEF TRADE WAS TOO EARLY

April 8 already showed how fragile the relief trade was. Brent plunged to $94.75 and the S&P 500 jumped 2.5% after the original two-week ceasefire was announced. A few days later, hopes of reopening pushed Brent down to $90.38 on April 17. But that optimism depended on ships actually moving. By April 21, only three ships had passed through Hormuz in the prior 24 hours, a tiny fraction of normal traffic.

For airline stocks, the shipping bottleneck matters more than the ceasefire headline itself. Delta expected about $2 billion of extra fuel costs in the June quarter and roughly $4.30-per-gallon jet fuel. Fuel is typically about 27% of airline operating expense. Until crude and refined products normalize, carriers such as Delta, United and American remain hostage to the same squeeze.

MAIN RISK

A faster diplomatic breakthrough is the biggest risk to this cautious view. If Washington eases the blockade, Iran returns to talks, and ship traffic restarts cleanly, Brent can drop sharply and airline stocks can rally hard because positioning has already turned defensive. A second risk is political: traders may keep fading every escalation on the view that Trump will keep delaying a worst-case outcome.

BASE CASE

Base case, this stays messy. The ceasefire extension buys time, but it does not yet remove the supply-chain friction that keeps oil elevated. For investors, that argues against treating this as a broad risk-on green light. Integrated oil and refining names still have cleaner near-term leverage to a stubborn crude premium, while airlines and cruise operators need proof that shipping, fuel inventories and pricing are actually normalizing before the relief trade is durable.

Q&A

- Does the ceasefire extension make airline stocks a buy today?

- Which metric matters most now?

- What is the biggest misunderstanding in this setup?

- What would change the call?