Tesla Q1 Beats, But Slides as Capex Seen Jumping ~300%

Tesla beats Q1 earnings expectations but sees shares slide as investors worry about a massive capital expenditure surge that could pressure near-term cash flow.

Tesla kicked off the “Magnificent Seven” earnings season with a headline beat—but what began as a clean upside surprise quickly morphed into a market reset.

Strong margins, surging free cash flow, and resilient demand were overshadowed by one critical shift: an aggressive, capital-intensive future that may weigh on near-term cash generation.

📊 Q1 Performance: A High-Quality Beat

Tesla delivered a broadly strong quarter across key financial metrics.

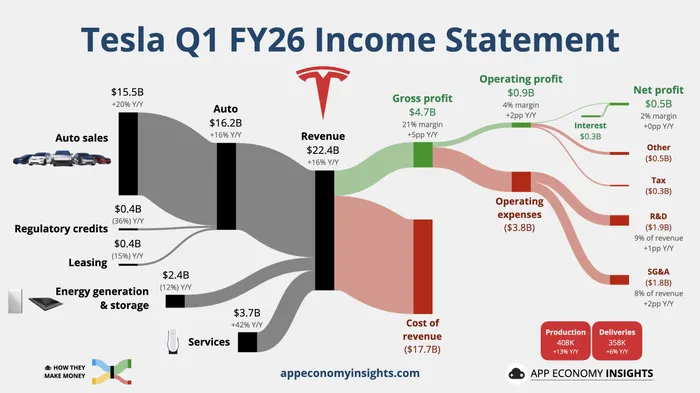

Revenue reached $22.387 billion, up 16% year-over-year, slightly below the $22.8 billion consensus but still reflecting solid top-line growth.

Non-GAAP EPS came in at $0.41, marking a 52% YoY increase and comfortably beating the $0.34 expectation.

Profitability also surprised to the upside. Gross margin expanded from 20.1% in Q4 to 21.1%, far exceeding the market’s 17.7% estimate—signaling improved cost control and pricing dynamics.

Free cash flow surged to $1.444 billion, up 117% YoY, versus expectations of a -$1.86 billion outflow. Lower-than-expected capital expenditures were the key driver behind this outperformance.

🧩 Business Breakdown: Services Take the Lead

Under the surface, Tesla’s growth mix is evolving.

The automotive segment, still the core business, generated $16.234 billion in revenue, up 16% YoY. Notably, reputational headwinds linked to DOGE appear to be fading, with a visible recovery in European demand.

The energy generation and storage segment delivered $2.408 billion, down 12% YoY, reflecting timing-related volatility rather than structural weakness.

Meanwhile, services revenue jumped 42% YoY to $3.745 billion, emerging as the standout contributor this quarter. This reinforces Tesla’s gradual pivot toward higher-margin, recurring revenue streams.

🎢 Market Reaction: From Euphoria to Repricing

Initial market reaction was decisively positive. Tesla shares rose nearly 5% after hours following the earnings release.

However, sentiment reversed sharply during the earnings call.

CFO Vaibhav Taneja disclosed that 2026 capital expenditures are expected to exceed $25 billion, nearly tripling from $9 billion in 2025. This dramatic increase implies that free cash flow could turn negative over the remainder of this year.

Elon Musk reinforced the shift, stating Tesla would significantly increase investment to capture long-term opportunities, expecting substantial future returns.

The market quickly repriced the stock—shares erased gains and turned negative as investors recalibrated expectations from profitability to capital intensity.

🚗 Automotive Strategy: From Volume to Platform

Tesla’s automotive narrative is undergoing a structural transition.

The company continues to optimize its lineup, advancing more affordable versions of Model 3 and Model Y, alongside the new Model YL. The Cybertruck has already begun deliveries in the UAE, signaling international expansion.

Looking ahead, Tesla expects Robotaxi-compatible Cybercab and the Semi truck to enter mass production this year, while the long-awaited Roadster could debut within roughly a month.

This signals a clear shift: from selling vehicles at scale → to deploying fleets and monetizing mobility services.

🤖 Autonomy: Building the FSD Flywheel

Full Self-Driving (FSD) is becoming a central pillar of Tesla’s monetization strategy.

FSD subscriptions reached 1.28 million, growing 51% YoY and 16% sequentially. Tesla has eliminated one-time purchases, moving entirely to a subscription model to enhance recurring revenue and adoption.

While Musk expects limited revenue contribution from FSD this year, he anticipates a meaningful ramp starting in 2026.

On the regulatory front, supervised FSD received approval in the Netherlands in April, potentially paving the way for broader EU adoption. Tesla plans to begin rolling out unsupervised FSD in Q4, subject to regional safety validation.

However, hardware constraints remain. Existing HW3 systems are no longer sufficient, prompting Tesla to establish micro-factories in major cities to upgrade vehicles.

🚕 Robotaxi: Scaling, but Not Frictionless

Tesla’s Robotaxi ambitions are progressing steadily.

Paid Robotaxi mileage nearly doubled quarter-over-quarter, and in April, fully driverless operations (without safety monitors) expanded to Dallas and Houston, with continued scaling in Austin.

Importantly, Tesla reports zero injury incidents to date.

That said, the primary bottlenecks are operational rather than safety-related—such as handling traffic edge cases and navigating temporary obstacles. These limitations continue to constrain large-scale deployment.

🦾 Optimus: The Long-Term Wildcard

Elon Musk positioned the Optimus humanoid robot as Tesla’s most important product ever, even surpassing its automotive business.

The company is repurposing its Fremont Model S/X production lines into an Optimus factory, with production expected to begin in August and a target capacity of 1 million units annually.

However, initial output will be limited due to the complexity of over 10,000 newly designed components.

The Optimus V3 design is nearly complete, though its unveiling may be delayed to protect intellectual property.

A second Optimus factory in Austin is scheduled for 2027, with an ambitious long-term capacity target of 10 million units per year.

⚡ Energy & Infrastructure: The Silent Growth Engine

Tesla’s energy business remains volatile quarter-to-quarter but structurally compelling.

The Houston-area Megafactory continues to progress and is expected to begin producing Megapack 3 systems later this year.

Meanwhile, Tesla has started scaling deliveries of its in-house designed solar panels from its New York facility. These panels feature 18 independent generation zones, enabling superior performance under partial shading, along with improved aesthetics and simplified installation.

On the supply chain side, Tesla is ramping LFP battery production in Nevada and expanding into cathode materials and lithium refining in Texas. Still, the company emphasized that battery pack capacity remains the key bottleneck for vehicle production growth.

🧠 AI & Chips: The Strategic Endgame

Beyond vehicles and energy, Tesla is quietly building an AI infrastructure layer.

In collaboration with SpaceX, the company aims to develop what it describes as the largest chip factory in history, starting with a research-oriented wafer fab in Texas.

Tesla confirmed that its next-generation AI inference chip taped out in April, while the AI5 chip has already completed tape-out ahead of schedule—highlighting rapid progress in its custom silicon roadmap.

🧭 Conclusion: From Earnings Story to Capital Story

Tesla’s Q1 results were objectively strong—beating expectations across earnings, margins, and cash flow.

But the market is no longer focused on what Tesla delivered— it is focused on what Tesla is about to spend.

The narrative is shifting:

Short term: Rising capex, potential free cash flow pressure

Long term: Massive optionality in autonomy, robotics, and AI infrastructure

👉 Tesla is no longer being priced purely as a car company. 👉 It is evolving into a capital-intensive platform bet on AI-driven physical systems.

And that transition comes with both extraordinary upside—and near-term valuation friction.