Intel Rallies 20% on Q1 Beat, CPU Giant Back!

Intel shares surge nearly 20% after crushing Q1 earnings and raising guidance, signaling a credible recovery driven by surging AI demand and manufacturing progress.

Intel’s latest earnings didn’t just beat expectations—they reshaped the narrative. After years of skepticism, the company delivered a decisive Q1 surprise alongside a stronger-than-expected outlook, signaling that the long-declining CPU giant may finally be entering a credible recovery phase.

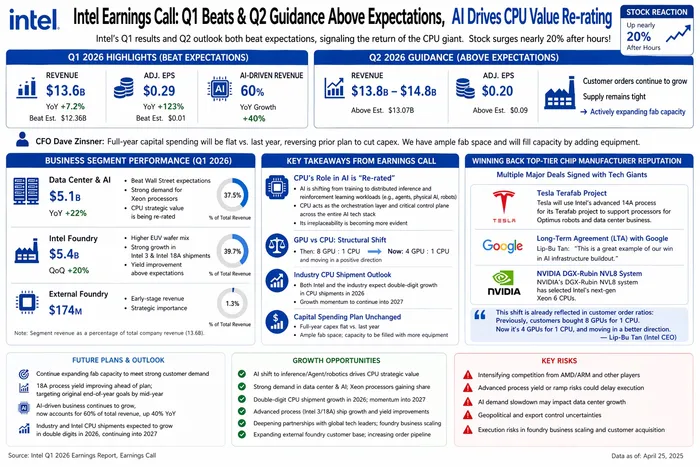

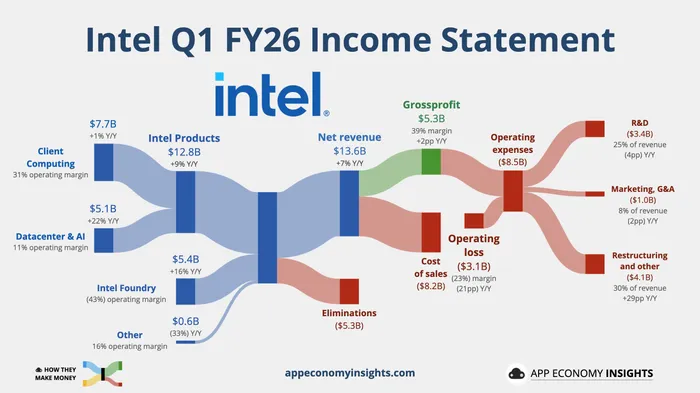

At the core of this optimism is a clean and convincing financial performance. Intel reported Q1 revenue of $13.6 billion, up 7.2% year-over-year and well above the $12.36 billion consensus. Profitability delivered an even stronger signal. Adjusted earnings per share came in at $0.29, marking a 123% increase from a year ago and crushing expectations of just $0.01.

This was not a marginal beat—it was a broad-based upside surprise across both revenue and earnings, suggesting that underlying demand has strengthened meaningfully.

More importantly, forward guidance reinforced that momentum is not fading. Intel expects second-quarter revenue in the range of $13.8 billion to $14.8 billion, comfortably ahead of the $13.07 billion market forecast. Adjusted EPS is projected at $0.20, more than double the $0.09 consensus. Management pointed to sustained strength in customer orders, noting that demand continues to outpace supply. In response, the company is accelerating efforts to expand capacity, underscoring confidence in the durability of the recovery.

The market response was immediate: shares surged nearly 20% in after-hours trading, reflecting a sharp shift in investor sentiment.

That confidence is also evident in Intel’s capital allocation strategy. CFO Dave Zinsner revealed that full-year capital expenditures will remain in line with last year, reversing earlier plans to cut spending. Rather than scaling back, Intel is leaning into expansion—leveraging its existing factory footprint while increasing equipment investment to unlock additional capacity. This decision reflects a clear strategic stance: prioritize growth and execution over short-term margin preservation.

Driving much of this resurgence is Intel’s growing exposure to artificial intelligence. AI-related businesses now account for roughly 60% of total revenue and are growing at a 40% annual pace. This is not just a cyclical boost—it reflects a deeper structural shift in how compute demand is evolving. Within this context, Intel’s Data Center and AI segment delivered $5.1 billion in revenue, up 22% year-over-year and ahead of expectations, with demand for its flagship Xeon processors continuing to strengthen.

Crucially, Intel is benefiting from a redefinition of the CPU’s role in the AI stack. As workloads shift from large-scale training to distributed inference and reinforcement learning applications—such as AI agents, physical AI systems, and robotics—the CPU is increasingly positioned as the orchestration layer and control plane of computing infrastructure. This shift is already visible in purchasing behavior. Where customers previously bought one CPU for every eight GPUs, that ratio has improved to one for every four GPUs, and continues to trend upward. Intel expects double-digit CPU shipment growth this year, with momentum extending through 2027.

At the same time, Intel is making tangible progress in restoring its manufacturing leadership. The company has secured multiple high-profile deals and long-term agreements with major technology players, including Google. It is also gaining traction across the broader ecosystem. Tesla plans to adopt Intel’s advanced 14A process for its Optimus robotics and data center chips, while NVIDIA’s DGX-Rubin NVL8 system will incorporate Intel’s next-generation Xeon 6 processors. These wins signal renewed confidence in Intel’s process roadmap and execution capabilities.

Internally, manufacturing metrics are also improving. Intel’s foundry business generated $5.4 billion in revenue during the quarter, up 20% sequentially, driven by a higher mix of EUV wafers and strong ramp-up in Intel 3 and Intel 18A nodes. External foundry revenue reached $174 million. Perhaps most notably, yield improvements on the critical 18A process are ahead of schedule. Levels initially expected by year-end are now projected to be achieved by mid-year, suggesting that execution risks—long a key concern for investors—may be easing.

Taken together, Intel’s latest results mark a meaningful turning point. The company is no longer defined solely by past missteps, but increasingly by its positioning in the next phase of computing—where AI, infrastructure, and manufacturing converge. The combination of strong financial performance, improving demand dynamics, and credible execution progress has begun to rebuild market confidence.

The question now is not whether Intel can stage a recovery—it already is. The real test is whether it can sustain this momentum, scale its advantages, and fully reestablish itself as a leader in the AI-driven semiconductor landscape.