Texas Instruments'19% Jump Signals a Broader Chip Trade Beyond AI

Texas Instruments surged 19% on strong earnings, signaling a potential semiconductor recovery beyond AI despite broader market weakness.

Texas Instruments became the cleanest earnings signal in a messy Thursday session. Shares rose 19.4% on April 23, the strongest upward force inside the S&P 500, even as the Nasdaq Composite fell 0.9% and the S&P 500 slipped 0.4%.

Closing levels confirmed the split rather than a broad risk-on day. The S&P 500 ended at 7,108.40, the Dow Jones Industrial Average at 49,310.32 and the Nasdaq Composite at 24,438.50. Oil and Treasury yields were also part of the backdrop, with Brent crude briefly above $107 and the 10-year Treasury yield rising to 4.32% from 4.30% late Wednesday.

A Beat That Moved The Forward Bar

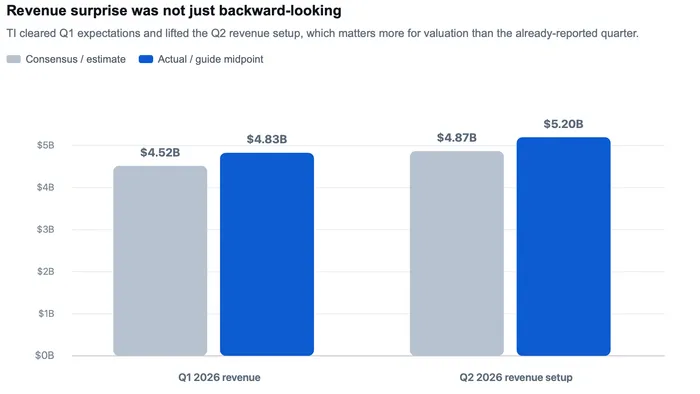

The size of the surprise becomes clearer when compared with expectations. LSEG consensus data cited by Reuters put Q1 revenue expectations at $4.53 billion and Q2 revenue expectations at $4.86 billion. Against that setup, TI's $4.83 billion Q1 revenue and $5.20 billion Q2 midpoint suggested that demand was improving faster than investors had priced in.

Source scope: Q1 reported revenue and Q2 guidance are from Texas Instruments; consensus and estimate figures are LSEG data cited by Reuters via Investing.com. Figures are in U.S. dollars.

Analog Breadth Is The Real Signal

TI's Analog revenue rose 22% from a year earlier to $3.92 billion, Embedded Processing revenue rose 12% to $723 million and operating profit increased 37% to $1.81 billion, according to the company's earnings release. Growth led by industrial and data-center customers carries more weight for investors than a narrow consumer-electronics bounce. During the Q1 call transcript, executives described broad demand across sectors and regions but also said the second half remained unknown. That caution matters: a durable rerating needs evidence that orders are not merely catching up after customers ran lean inventory.

Nasdaq Read-Through Depends On Quality Of Growth

For Nasdaq investors, Thursday's session drew a sharper line between companies getting credit for visible demand and companies being penalized for heavier spending or softer growth details. AP's market report showed Tesla, IBM and ServiceNow weighing on the tape while Texas Instruments offset part of the pressure. Stock selection inside technology therefore mattered more than index direction.

Analog chips sit closer to industrial production, power management, autos and data-center infrastructure than to the most crowded software multiple trade. A stronger TI print suggests parts of the semiconductor complex may be moving from inventory repair toward demand confirmation. Nasdaq leadership becomes healthier if earnings support spreads beyond a small cluster of megacap stories; it becomes more fragile if Thursday's TXN move proves to be an isolated earnings squeeze.

Margin And Cash Flow Still Have To Validate The Repricing

TI reported $7.82 billion of trailing-12-month operating cash flow and $4.35 billion of free cash flow, while returning $6.03 billion to shareholders over the same period, the company said in its release. Those figures support the idea that better demand can pass through to shareholder economics, not just sales growth.

Capacity investment complicates the margin story. TI spent $4.1 billion on capital expenditures over the past 12 months, and the market still has to judge whether internal manufacturing scale will create enough cost and supply-chain advantage to offset depreciation and cycle risk. A higher multiple needs proof that revenue growth is converting into sustainable gross profit and free cash flow, not just a temporary lift from scarce supply.

What The Market Has Already Priced In

Thursday's 19.4% gain appears to have priced in a near-term analog recovery, a stronger Q2 revenue base and better confidence that industrial and data-center demand can support estimates. With TI now acting as a positive force inside a weaker S&P 500 session, investors have also priced in some probability that the semiconductor trade is broadening rather than depending only on the most obvious infrastructure winners.

- What could still surprise investors? Upside would come from Q2 orders confirming that industrial customers are rebuilding demand rather than just normalizing inventory, with data-center power demand remaining strong into the second half. Downside would come from any sign that the Q2 guide pulled demand forward, that auto remains uneven, or that higher factory and assembly investments slow the free-cash-flow improvement investors are now assuming.

- What should traders and long-term investors watch next? Traders should monitor whether TXN can hold leadership while the Nasdaq absorbs higher oil, a firmer 10-year Treasury yield and weak reactions in other technology earnings. Longer-term investors should focus on Q2 revenue conversion, Analog margin, inventory days, order breadth across industrial and auto customers, and management's next comments on whether data-center power demand is becoming a recurring revenue driver rather than a one-quarter acceleration.