Wilmar FY2025: Strong Profit Growth Masks Capital Return Strain

Wilmar's FY2025 numbers on the surface tell a story of robust growth. Total revenue climbed 5% to US$70.42 billion, while EBITDA rose 10% to US$4.27 billion. Net profit posted the strongest gain at 21% to US$1.41 billion. Yet beneath these headline figures lies the central tension investors must grapple with: the quality of that profit growth and what it means for capital returns.

The net profit surge was significantly boosted by one-off items. After adjusting for non-core gains and provisions totaling US$103.8 million-primarily a large gain on remeasurement from a change in interest in AWL Agri Business Limited, offset by provisions for Indonesia operations, legal cases in China, and a loss in Pakistan-the core net profit stands at US$1.28 billion, up 10%. This is the more sustainable earnings picture, and it's notably more modest than the 21% net profit growth suggests.

More telling for the capital return thesis is the dividend decision. The board proposed a final dividend bringing the total payout to S$0.140 per share, a 13% reduction year-on-year. This cut comes even as the stock rallied to a new 52-week high of $31.45 earlier this month trading intraday as high as $31.45. For a company with a vertically integrated model spanning origination, processing, and distribution, the move signals that internal capital needs are taking precedence. The net debt-to-equity ratio sits at 0.91x, indicating elevated leverage that limits financial flexibility Net Debt/Equity at 0.91x.

The bottom line: Wilmar delivered solid operational profit growth, but the market's celebration of the stock hitting a new high may be overlooking the strain on its capacity to return capital. Investors weighing the recent price appreciation against a material dividend cut and a leveraged balance sheet are being presented with a classic quality-of-earnings question. The one-off gains masked the underlying pressure on cash flows available for shareholders.

Profit Quality and One-Off Drivers

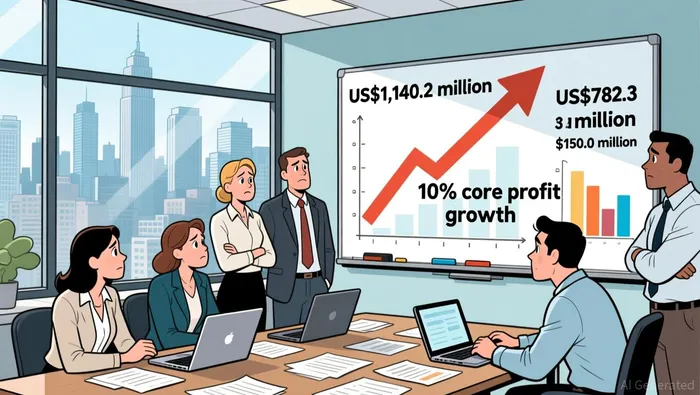

The 21% net profit growth headline masks a more nuanced reality. To assess the sustainability of Wilmar's earnings, we must dissect the one-off adjustments that swelled the bottom line. The net effect of these non-core items was a gain of US$103.8 million, but the gross movements were far more dramatic, canceling each other out to a significant degree.

The primary driver was a substantial one-time gain. The group recognized a gain on remeasurement of US$1,140.2 million arising from a change in interest in AWL Agri Business Limited. This non-cash accounting gain provided a major boost to reported profits. However, it was partially offset by a series of significant provisions and compensation payments elsewhere in the business. The largest of these was US$(782.3) million in compensation and provisions related to Indonesia operations. Further reductions came from a US$(104.1) million provision for ongoing legal cases in China and a US$(150.0) million provision for losses related to an associated company in Pakistan.

When these items are stripped away, the underlying operational performance becomes clearer. The core net profit stands at US$1.28 billion, representing a 10% year-on-year increase. This is the more reliable indicator of business health, as it reflects the sustainable earning power of Wilmar's vertically integrated model without the distortion of large, irregular items. The 10% core growth is solid, but it is half the rate of the headline net profit surge. For investors, this decomposition is crucial: the one-off gains provided a temporary lift, while the real test is whether this underlying profit base can be maintained and grown. The significant provisions, particularly in Indonesia and China, also serve as a reminder of the operational and regulatory risks that can materialize unexpectedly in a complex, global business.

Balance Sheet and Liquidity Position

Wilmar's balance sheet shows a company carefully calibrating its capital structure, with modest leverage improvements but liquidity constraints that shape strategic choices.

The net debt-to-equity ratio improved from 0.94x to 0.91x in FY2025, marking incremental progress in managing leverage Net Debt/Equity at 0.91x. Yet this metric alone doesn't capture the full picture. The quick ratio of 0.67 and current ratio of 1.12 reveal modest liquidity buffers-particularly the quick ratio, which sits below the 1.0 threshold often seen as a safety margin quick ratio 0.67, current ratio 1.12.

A notable discrepancy warrants attention: while the financial statements report net debt-to-equity at 0.91x, trading data references a debt-to-equity ratio of 0.29 debt-to-equity 0.29. This likely reflects different measurement scopes-the former accounting for cash and cash equivalents netted against debt, the latter using gross debt. Both metrics, however, point to a company managing meaningful leverage in service of its integrated model.

The dividend cut from S$0.161 to S$0.140-a 13% reduction-becomes more understandable when viewed against this liquidity backdrop Dividends per share S$ 0.140. Management appears to be prioritizing balance sheet strength over shareholder returns, a prudent stance given the capital-intensive nature of Wilmar's vertically integrated operations.

The strategic choice is clear: preserve financial flexibility for future opportunities and operational needs rather than maximizing near-term distributions. For investors, this raises the question of whether the recent stock price appreciation-reaching a 52-week high at $31.45 trading intraday as high as $31.45-is justified given the constraints on capital returns. The balance sheet suggests management is playing the long game, building resilience in an uncertain commodity environment.

What to Watch: Catalysts and Risks

The FY2025 results set the stage, but the next few quarters will determine whether Wilmar's story is one of sustainable improvement or continued masking of underlying pressures. Several forward-looking factors will be critical for investors tracking this thesis.

The first test arrives with Q1 2026 results, expected around May 2026. This quarter will show whether core profit growth of 10% can be sustained without the one-off tailwinds that boosted FY2025 quarterly investor presentations. The market will be looking for confirmation that the underlying operational engine is robust enough to deliver consistent earnings, rather than relying on occasional accounting gains. Any deterioration in the 10% core growth trajectory would signal that the profit quality concerns raised in this analysis are more than just temporary distortions.

Commodity price movements represent the next major variable. Wilmar's vertically integrated model spans the entire value chain, from origination through processing to distribution, which means it carries inherent exposure to commodity cycle swings quarterly investor presentations. If palm oil and edible oil input costs rise sustainably, margins across the processing and trading segments could come under pressure. The company's ability to pass through higher costs to customers, or to hedge effectively, will be closely watched. A sustained period of elevated commodity prices could test the margin resilience that investors are assuming is built into the integrated model.

On the capital return front, the 13% dividend cut was a clear signal of management's prioritization of balance sheet strength over shareholder distributions quarterly investor presentations. For a return to growing payouts, investors should expect to see either sustained core profit expansion beyond the current 10% trajectory or meaningful debt reduction. The net debt-to-equity ratio of 0.91x remains elevated for a company of Wilmar's scale, and the quick ratio of 0.67 suggests liquidity remains tight quarterly investor presentations. Any shift in this policy will likely be gradual, tied to demonstrable improvement in these underlying metrics.

Regional operational risks in Indonesia and China cannot be overlooked. The substantial provisions taken in FY2025-US$(782.3) million for Indonesia and US$(104.1) million for China-reflect real regulatory and legal exposures quarterly investor presentations. If regulatory environments tighten further or legal cases extend beyond current expectations, additional provisions could materialize, catching investors off guard. The Pakistan loss related to an associated company (US$(150.0) million) adds another layer of regional risk to monitor quarterly investor presentations.

The key question for investors is whether the recent stock price appreciation to 52-week highs is justified by the fundamental outlook. The balance sheet constraints, dividend cut, and commodity exposure suggest caution is warranted. The next few quarters will provide the data needed to answer whether Wilmar's integrated model is delivering the resilience it promises, or whether the profit growth story remains more fragile than the headline numbers suggest.