SNDK Earnings Preview. The Pullback Didn't Kill the Hype

Sandisk faces a critical earnings test as investors scrutinize whether AI-driven data center demand sustains beyond fiscal Q3 peak expectations.

Sandisk will report fiscal third-quarter results on April 30, 2026, after announcing a 1:30 p.m. Pacific Time conference call. The company enters the report after a sharp rerating and a fresh pre-earnings pullback, helped by its pure-play NAND profile, stronger data-center demand and inclusion in the Nasdaq-100 before the April 20 open.

Latest market data also changes the tone of the setup. Sandisk closed at $1,002.35 on April 28, down 6.34% from the prior session after closing at $1,070.20 on April 27. The drop does not weaken the NAND thesis, but it shows investors are becoming more selective before earnings. A strong Q3 may already be expected; guidance quality is now the real test.

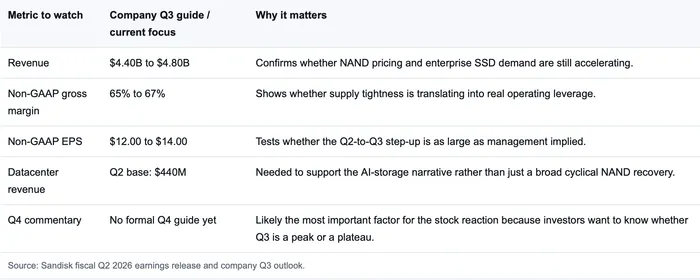

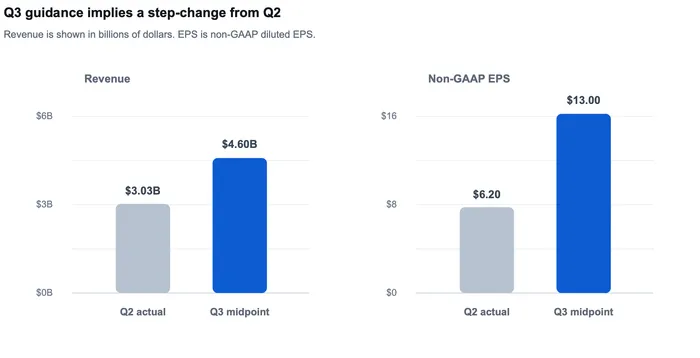

Fiscal Q2 already showed why investors are paying attention. Sandisk reported revenue of $3.03 billion, up 61% year over year, with non-GAAP gross margin of 51.1% and non-GAAP diluted EPS of $6.20. More important for the current trade, management guided fiscal Q3 revenue to $4.40 billion to $4.80 billion and non-GAAP diluted EPS to $12.00 to $14.00. That means the market is not waiting for a normal beat; even after the April 28 pullback, it is still pricing in a major earnings reset.

What Investors Need From Q3

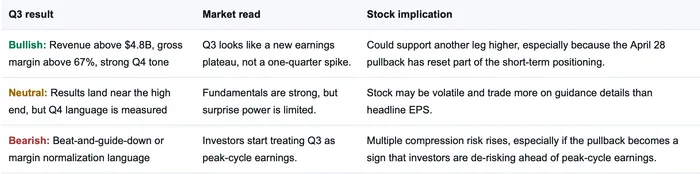

A clean bullish read would require revenue above the high end of guidance, gross margin at or above the 65% to 67% range, and management language suggesting strong pricing can continue into fiscal Q4. A merely good quarter may not be enough if the call sounds cautious. For a stock that has already become a high-expectation AI-storage proxy, the key question is durability.

- Source: Sandisk fiscal Q2 actual results and fiscal Q3 guidance from the company's earnings release. Q3 uses midpoint guidance.

AI Storage Could Become a Real Earnings Driver

SNDK's strongest argument is that AI infrastructure is widening beyond GPUs and high-bandwidth memory. Training and inference workloads need storage capacity, fast access and reliable data movement. Sandisk is well positioned because enterprise SSD demand can benefit from both AI data-center spending and broader NAND pricing strength.

Q2 already gave investors a visible signal. Datacenter revenue reached $440 million, up 64% sequentially and 76% year over year, while Edge and Consumer revenue also improved. That mix matters: if datacenter keeps scaling, the market can treat Sandisk as more than a cyclical memory rebound. A larger, more durable enterprise SSD business would support higher normalized earnings and a stronger multiple.

Great Numbers Could Still Look Peak-Like

Weak Q3 earnings are not the main risk. A bigger concern is that investors later define Q3 as the peak of the cycle. Memory stocks often look cheapest when earnings are temporarily strongest. If management signals margin normalization, weaker follow-through from enterprise customers or faster supply response from the industry, the market could compress the multiple even if the printed quarter beats guidance.

Another point deserves attention: Sandisk's manufacturing structure gives it supply access, but it also brings fixed-cost exposure. The company's fiscal Q2 Form 10-Q described Flash Ventures obligations and disclosed material exposure tied to the joint venture structure. That is not an immediate balance-sheet alarm, but it is a reminder that operating leverage works in both directions when the cycle turns.

Likely Stock Reaction Framework

Simple Investment View

SNDK is still a strong fundamental story, and the latest pullback slightly improves the entry point. Even so, the pre-earnings risk/reward looks more balanced than early in the rerating. A positive stance depends on Q3 showing that enterprise SSD demand and NAND pricing strength can last into future quarters. Without that evidence, the stock is vulnerable to a "good quarter, not good enough" reaction.

A practical way to frame the setup is Hold / Watch for guidance. Existing holders can justify staying involved if Q4 commentary remains firm and datacenter growth keeps improving. New buyers may still need a cleaner entry point or stronger proof that fiscal Q3 is not close to peak earnings. The report is therefore less about whether Sandisk is a good company and more about whether the current valuation already assumes the best part of the cycle.