OpenAI Misses Targets! SoftBank Plummets 9.86%, Oracle Drops 4.05%: Is the AI Compute Chain Collapsing?

OpenAI misses revenue targets, triggering a global AI selloff that erases billions and forces a sector-wide shift from speculative growth to fundamental earnings validation.

OpenAI's recently reported failure to meet pivotal internal user and revenue benchmarks has sent immediate shockwaves through global equities, highlighting escalating concerns over the return timeline for massive artificial intelligence compute investments. On April 28, 2026, disclosures revealed mounting internal doubts regarding the firm's ability to fund its aggressive future data center expansions. This fundamental revelation instantly pulled down major AI-linked hardware and software equities worldwide, erasing billions in market capitalization practically overnight. My analytical stance on this development is decisive: this sector-wide correction is a structurally healthy recalibration. It forces institutional capital to transition away from speculative capacity hoarding and instead demand fundamental earnings validation, ultimately fortifying the long-term sustainability of the semiconductor and data center ecosystems.

Unpacking the Internal Misses and Financial Constraints

The epicenter of this market event stems from the organization missing critical operational metrics. By the close of last year, OpenAI failed to achieve its internal objective of securing one billion weekly active users for ChatGPT. Financial velocity also decelerated, with the firm missing its yearly revenue targets as Google's Gemini platform experienced massive growth and aggressively captured market share. Furthermore, OpenAI missed multiple monthly revenue targets early this year, losing crucial ground in the enterprise and coding sectors to competitors.

These growth shortfalls have generated severe internal financial friction. Chief Financial Officer Sarah Friar has explicitly communicated concerns to executive leadership regarding the company's capacity to pay for future computing contracts if the current revenue trajectory fails to accelerate. The financial stakes are staggering, considering CEO Sam Altman embarked on a strategy last year that put the firm on the hook for approximately $600 billion in future spending commitments. Consequently, the board of directors has intensified its scrutiny of these massive data-center deals, actively questioning Altman’s push to acquire even more computing power despite clear signs of a business slowdown. While the company recently fortified its balance sheet by raising $122 billion, internal projections suggest they will burn through that capital within three years—and that assumes they meet their highly ambitious revenue targets. In response, executives are now pushing for stringent cost controls and operational discipline, placing them at odds with the CEO's expansive strategy.

Market Contagion: The Compute Hardware Selloff

The public exposure of these internal operational struggles triggered an immediate and aggressive market reaction. The Nasdaq composite registered a decline of over 1% earlier in the session following reports from The Wall Street Journal regarding the internal rift. However, the most severe technical damage was isolated to the specific companies serving as the hardware and capital backbone of the generative AI sector.

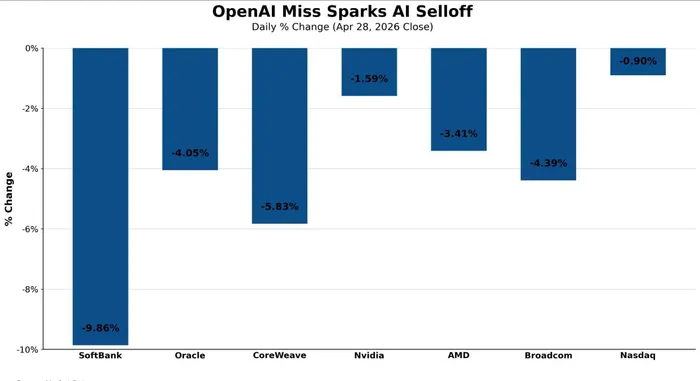

According to Ainvest analysis mapping the daily percentage change at the April 28, 2026 close, the sector witnessed sweeping distribution. Global technology conglomerate SoftBank Group, which has committed an excess of $60 billion to OpenAI, recorded a precipitous 9.86% drop in Tokyo trading as investors digested the risk exposure. Major compute infrastructure partner Oracle experienced a sharp 4.05% decrease. The collateral damage extended heavily into other cloud infrastructure and semiconductor equities. CoreWeave recorded a steep 5.83% drop, while Broadcom fell 4.39%. Even the undisputed sector bellwethers could not evade the downward momentum, with Advanced Micro Devices (AMD) sliding 3.41% and Nvidia posting a 1.59% decline. These immediate price actions demonstrate rapid portfolio de-risking, as algorithmic and institutional traders assessed that cash flow constraints at the primary AI buyer would mechanically imperil the forward revenue streams of its infrastructure vendors.

Repricing the Anchor of the AI Narrative

To properly quantify the severity of this market reaction, analysts must recognize OpenAI's position not merely as a prominent software vendor, but as the foundational anchor of the entire global artificial intelligence investment narrative. Over the past two years, Altman's aggressive procurement strategy successfully tied much of the broader technology sector's success directly to OpenAI’s expansion trajectory. This "buy everything" computing paradigm was fundamentally buoyed by the perception of ChatGPT’s invincible market dominance.

When the apex buyer of global processing power signals a potential cash flow bottleneck and slowing user adoption, the market is forced to instantaneously reprice the entire infrastructure value chain. Market participants are no longer modeling for infinite, price-inelastic demand for high-performance processors and hyperscale data centers. Instead, they are recalibrating the certainty of future silicon orders, capital expenditure delivery timelines, and forward earnings multiples for the entire hardware ecosystem. If spending scrutiny forces OpenAI to rationalize its $600 billion in commitments, the subsequent ripple effects will aggressively alter the consensus revenue forecasts for semiconductor foundries, memory manufacturers, and server assemblers. This marks a definitive transition phase: the market is rotating from a macro-narrative driven expansion into a micro-earnings driven environment, where tangible return on invested capital dictates asset pricing.

Future Outlook: IPO Timelines and Sector Resilience

Looking ahead, the heightened financial scrutiny presents complex variables for technology investors, particularly regarding OpenAI's highly anticipated public market debut. The current friction over expenditures is actively constraining management's ambitions ahead of a potential initial public offering that could occur by the end of the year. Internal divisions exist regarding this timeline; while Altman favors an aggressive IPO schedule, Friar has expressed strong reservations. She has cautioned the board that internal controls must be heavily fortified, noting the company is not yet ready to meet the rigorous regulatory and reporting standards required of a publicly traded entity.

However, equity investors must separate OpenAI's specific corporate maturation challenges from the broader secular trend of enterprise AI adoption. While OpenAI shifts focus toward cost reduction—such as scaling back projects like its video-generation app Sora to support the rapidly growing Codex tool—the broader industry structure remains incredibly robust. It is critical to note that rival firm Anthropic has now reportedly achieved a secondary valuation exceeding $1 trillion. This massive capital allocation indicates that institutional liquidity continues to flow heavily into the sector, recognizing the vast enterprise utility of foundational models. Furthermore, OpenAI's recent release of the benchmark-topping GPT-5.5 model proves that core engineering execution has not stalled despite internal financial debates.

Conclusion

Ultimately, the current equity volatility stems from a vital shift in structural market expectations. This decline is not a single company's bearish news, but the market's reassessment of the return rhythm on AI capital expenditures. The era of unchecked compute accumulation is maturing into a cycle that strictly demands demonstrable revenue scaling and hardened operational discipline.