AI Capex Is No Longer Enough. Big Tech Now Has to Prove the Payback.

Big Tech stocks diverge as investors reward visible AI revenue conversion while penalizing heavy capex that threatens margins and free cash flow.

AI Spending Got a New Test

Four megacap technology reports after the April 29 close gave investors a cleaner way to judge the AI infrastructure trade: spend is still rising, but stocks are being sorted by visible revenue conversion, margin durability and cash-flow pressure.

Alphabet rose in after-hours trading while Meta, Microsoft and Amazon were lower in the same post-results window. That reaction should not be treated as a full verdict on the companies. It is better read as a sharper sorting mechanism: investors rewarded the cleanest visible payback and discounted cases where the spending bill, valuation, margin pressure or cash conversion still looked harder to underwrite.

Asset mapping is direct. Alphabet and Microsoft are being judged on cloud acceleration and AI product usage, Amazon on AWS growth versus free-cash-flow drag, Meta on whether advertising gains can carry another step-up in infrastructure spending, and the supplier chain on whether hyperscaler demand is durable enough to become recurring orders rather than a one-time capacity surge.

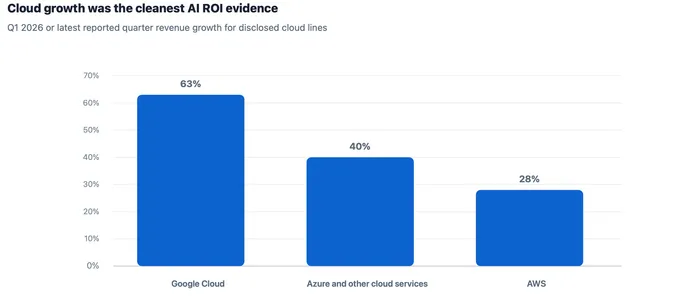

Source: company releases and filings from Alphabet, Microsoft and Amazon. Meta is discussed separately because it does not disclose a comparable cloud revenue segment.

Alphabet Showed the Cleanest Payback

Alphabet gave the market the clearest evidence that heavy AI investment can translate into operating data. Its SEC-filed earnings exhibitshowed consolidated revenue up 22% to $109.9 billion, operating margin expanding two percentage points to 36.1%, and Google Cloud revenue up 63% to $20.0 billion.

That combination matters because investors entered the print with two separate concerns: AI capex could dilute free cash flow, and AI answers could pressure search monetization. Alphabet did not settle either debate for the full year, but Search and other revenue rose 19% to $60.4 billion, and Google Cloud operating income increased to $6.6 billion from $2.2 billion a year earlier.

Pricing in Alphabet now looks less like a simple "spend more on AI" trade and more like a cloud-margin, backlog and search-resilience trade. Its own release said Google Cloud backlog nearly doubled quarter over quarter to more than $460 billion, giving investors a concrete validation metric for the next several quarters.

Microsoft Kept Azure at the Center

Microsoft's quarter also supported the demand side of the AI infrastructure story. Revenue rose 18% to $82.9 billion in the fiscal third quarter, Microsoft Cloud revenue rose 29% to $54.5 billion, and Azure and other cloud services revenue increased 40%.

Management's strongest data point was not only Azure growth. The company said its AI business surpassed a $37 billion annual revenue run rate, up 123% year over year. For a market worried about AI demand after the sector's spring rally, that is direct support for the idea that enterprise usage is still scaling.

Margin pressure remains part of the trade. Microsoft's performance page said gross margin percentage decreased because of continued AI infrastructure investment and growing AI product usage, partly offset by cloud efficiency gains. Investors are therefore paying for growth that is strong, but not costless.

After-hours weakness does not have to mean the market rejected Microsoft's AI demand story. A cleaner read is that expectations were already high, while investors still had to underwrite valuation, gross-margin dilution, ongoing capex needs and the risk that today's run-rate strength requires another round of infrastructure spending before it fully drops into free cash flow.

Amazon Added Scale With Cash Flow Pressure

Amazon's report gave the market a different version of the same setup. Net sales rose 17% to $181.5 billion in the first quarter, and AWS revenue increased 28% to $37.6 billion. AWS operating income rose to $14.2 billion from $11.5 billion a year earlier.

Scale is not the issue for Amazon. Cash conversion is. The company said trailing-12-month free cash flow decreased to $1.2 billion from $25.9 billion, driven primarily by a $59.3 billion year-over-year increase in property and equipment purchases, net of proceeds from sales and incentives. Amazon said that increase primarily reflected artificial-intelligence investments.

Investors therefore have to separate AWS demand from capital intensity. If AWS keeps accelerating and operating income holds, the capex burden looks like capacity investment. If growth fades while purchases remain elevated, the same numbers become a free-cash-flow reset.

Meta Showed Why Capex Still Carries a Penalty

Meta did not deliver a weak operating quarter. Revenue rose 33% to $56.31 billion, ad impressions increased 19%, average price per ad increased 12%, and free cash flow was $12.39 billion. Those figures point to a still-powerful advertising engine.

Yet the spend signal changed. Meta raised its 2026 capital expenditures outlook, including principal payments on finance leases, to $125 billion to $145 billion from the prior $115 billion to $135 billion range. The company attributed the increase to higher component pricing and, to a lesser extent, additional data-center costs to support future capacity.

For the stock, the expectation gap is clear. Meta's problem is not growth. Investors can see the bill more clearly than the next monetization layer. The market already understands that Meta can grow revenue while using AI to improve advertising relevance; less settled is whether the next layer of infrastructure spending produces enough incremental engagement, ad pricing or new product economics to keep free cash flow moving in the right direction.

Suppliers Still Need a Demand Signal

For AI suppliers, the read-through is constructive but not unconditional. Google Cloud, Azure and AWS growth support demand for Nvidia GPUs, custom accelerators, networking silicon, memory, power systems and data-center equipment. Hyperscaler spending plans still appear large enough to keep the supply chain busy.

Still, supplier stocks should not treat every capex increase as equally bullish. Nvidia and Broadcom have the cleanest link to sustained hyperscaler AI orders because they sit closer to accelerator and custom-chip demand. Micron is more exposed to whether HBM demand and pricing stay tight through the memory cycle. AMD needs evidence that its MI-series accelerators can keep taking cloud share rather than winning only episodic deployments.

Power, cooling and data-center equipment companies benefit from the total capex envelope, but they also carry a different risk profile. Higher component prices, grid bottlenecks, permitting delays or customer budget discipline can turn a bigger AI buildout into longer project timelines. Meta's update highlights that tension: suppliers may see higher revenue while customers become more sensitive to the cost of the next capacity round.

Validation Framework

Near-term validation now runs through four metrics. Alphabet needs continued Google Cloud margin strength and backlog conversion. Microsoft needs Azure growth and AI run-rate expansion without a deeper cloud-margin drawdown. Amazon needs AWS growth to translate into better free-cash-flow visibility. Meta needs evidence that higher capex lifts advertising efficiency, engagement or new AI revenue enough to justify the wider spending range.

Macro conditions still matter. Higher energy prices, tighter credit or rising equipment costs would make data-center buildouts harder to defend, especially for companies where the revenue conversion is less visible. A broad Nasdaq rally can keep the trade alive for a while, but the next earnings cycle will likely ask a more specific question: which AI budgets are earning their cost of capital?

For now, the priced-in view is that hyperscalers will keep spending and cloud demand remains strong. The less priced-in risk is dispersion inside the AI trade. Investors are no longer buying every dollar of AI capex equally. They are likely to reward three groups: companies that convert AI investment into cloud revenue, companies that defend gross margins and free cash flow, and suppliers that prove hyperscaler orders are not just inventory pulled forward. Companies with higher capex but no clear revenue loop may keep trading at a valuation discount.

Investor Q&A

- What changed after these earnings? AI capex is still large, but the market now has fresher evidence to separate cloud-backed spending from spending that depends on future payoff.

- Which assets are most exposed? GOOGL, MSFT, AMZN and META are the direct tests; NVDA, AMD, AVGO, MU, data-center power names and QQQ carry second-order exposure.

- What should investors track next? Google Cloud backlog conversion, Azure growth, AWS free cash flow, Meta's ad-price and engagement trends, and any change in component or data-center cost commentary.