Big Tech Earnings Preview: AI is Everything!

Microsoft, Google, Meta, and Amazon report earnings with zero margin for error as investors scrutinize AI investment returns rather than current profits.

After the market close, four members of the “Magnificent 7”—Microsoft, Google, Meta, and Amazon—will report Q1 earnings.

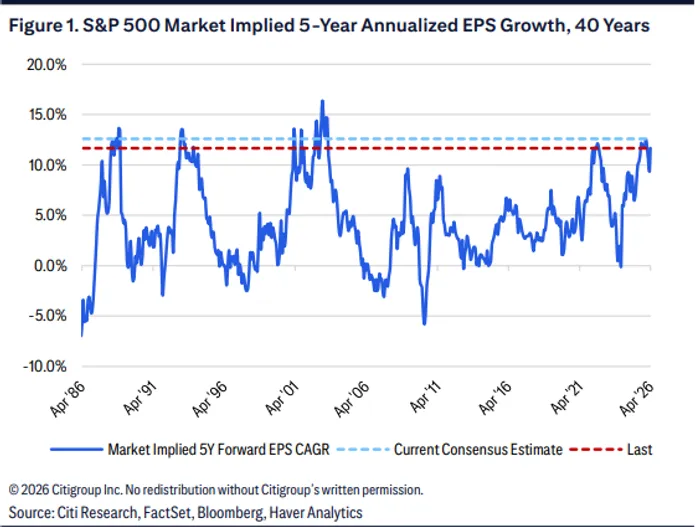

According to Citi strategist Scott Chronert and his team, current U.S. equity pricing implies a 5-year annualized EPS growth of 11.7%, very close to the consensus estimate of 12.6%.

This narrow gap highlights a critical point: There is virtually no margin for error in valuations, any sign of underperformance is likely to be harshly punished.

🧠 The Real Focus: Further Guidance, Not Q1 Result

The key question this earnings season is not Q1 performance—but forward guidance.

Tesla has already set the tone: despite beating across all Q1 metrics, its stock reversed sharply after Elon Musk signaled a significant increase in capital expenditures.

The message is clear: Big Tech must prove that AI-driven returns justify massive investment spending.

💻 Microsoft: Cloud Pressure Meets AI Competition

Microsoft has underperformed recently, with its core software business facing disruption from AI. Its stock has lagged the S&P 500, while competition intensifies—even from partners like OpenAI, as Microsoft gradually “decouples” from it amid rising rivalry from players like Anthropic.

This quarter, the spotlight is on Azure cloud performance.

Last quarter, Azure’s growth decelerated slightly, disappointing the market. Excluding OpenAI contributions, Azure’s backlog growth ranked lowest among the three major cloud providers (Azure, Google Cloud, AWS).

However, there is a constructive angle: Demand for compute continues to exceed supply, with capacity constraints being the primary bottleneck.

Microsoft’s CFO has maintained strict financial discipline, previously giving up significant power grid capacity—but this has now been corrected. As new capacity comes online, cloud growth is expected to reaccelerate.

Another key focus is Microsoft 365 and Copilot.

Enterprise productivity software is becoming highly competitive:

Anthropic continues to push aggressively

Gemini Enterprise AI is approaching 10 million users

👉 Microsoft must prove its ecosystem won’t be disrupted by AI.

🔍 Google: Ads + Cloud Drive Growth

Google’s two core pillars remain advertising and cloud.

Advertising revenue is expected to deliver double-digit growth, benefiting from deep integration with Gemini AI, query volume and session duration are rising; Ad targeting and conversion rates are improving. YouTube ads are supported by the monetization of Shorts.

On the cloud and AI front: Gemini monthly active users exceed 750 million, paid users grew 40% QoQ. Growth is driven by: Strong enterprise demand for AI infrastructure, rapid expansion of TPU leasing and acquisition of Wiz, enhancing cloud security capabilities

Additionally, Google’s in-house TPU chips significantly reduce reliance on NVIDIA GPUs—cutting costs and even enabling competition for customers.

📱 Meta: Can Ads Fund AI Ambitions?

For Meta, the core question is straightforward: Can advertising profits cover massive AI investments?

According to eMarketer April forecast, Meta’s 2026 ad revenue is expected to reach $243.46 billion, slightly surpassing Google’s $239.54 billion—making Meta the world’s largest digital advertising platform. Meta's market share is projected at 26.8%, edging out Google’s 26.4%.

eMarketer analyst Max Willens notes that Google’s dominance in search ads is weakening as AI reshapes user behavior. Product searches are shifting toward e-commerce platforms and AI assistants, with Google’s U.S. search ad share expected to fall below 50% for the first time.

Morgan Stanley surveys show that despite rising ad prices, SME advertiser demand for Meta remains resilient.

Cost discipline is also improving: 8,000 layoffs (~10% of workforce) and 6,000 open roles eliminated. At an estimated $150,000 median salary, this could save Meta roughly $1.2 billion annually.

🛒 Amazon: Monetizing AI Takes Time

Amazon CEO Andy Jassy has been explicit: Most AI capex in 2026 will be monetized in 2027–2028.

AWS added 3.9GW of power capacity in 2025, with total capacity expected to double by 2027, largely meeting customer demand.

The company’s Trainium3 chips also reduce reliance on NVIDIA, delivering significant cost savings.

Amazon’s advertising business is now the third-largest digital ad platform in the U.S., with strong growth momentum. Prime Video ads are rolling out at scale, advertiser budgets are recovering post-holiday. Q1 ad revenue is expected to grow at a double-digit pace.

On the e-commerce side: U.S. Q1 retail e-commerce grew >9% YoY (best in 3 years); Bank of America data shows 11% online consumption growth (vs. 8% in Q4); Online penetration exceeded 30%, up over 2 percentage points QoQ

As the global e-commerce leader, Amazon’s core business remains resilient and stable.