Top Rated Stocks: Tired of Mag7&Semis? Look Here

As Mag7 & semiconductor trades get crowded, the best opportunities are shifting to areas where fundamentals—not hype—are driving momentum.

HERE ARE OUR PICKS FOR THIS WEEK!

----------------------------------------------------------

IBM: AI-Native Reinvention Meets Quantum-Scale Industrial Disruption

IBM is reasserting itself as a high-leverage infrastructure play in the AI era, but the market still underestimates the compounding effect of its enterprise integration strategy. The collaboration with Dallara is not just a niche engineering story—it represents a broader shift toward AI-accelerated industrial design, where simulation cycles collapse from hours to minutes. This materially changes cost curves and innovation velocity across automotive and aerospace verticals.

More importantly, the launch of “IBM Bob” signals a decisive move into AI-first enterprise software orchestration. Unlike generic copilots, IBM is targeting full lifecycle ownership—from planning to deployment—embedding governance and compliance layers. This is critical because large enterprises are increasingly constrained not by AI capability, but by risk management and regulatory oversight.

From a financial lens, IBM’s hybrid cloud + AI segment continues to drive mid-single-digit revenue growth with expanding margins. The company trades at a discount to hyperscaler peers, yet delivers higher earnings stability and stronger free cash flow conversion. This creates a classic mispricing: lower growth perception, but higher monetization durability.

The quantum angle, while still long-dated, adds asymmetric optionality. If IBM successfully integrates quantum computing into real-world industrial workflows (as hinted in the Dallara case), it could unlock a new category of enterprise spending.

Verdict: IBM is transitioning from a legacy narrative to an AI infrastructure compounder, with underappreciated upside in enterprise AI and quantum integration.

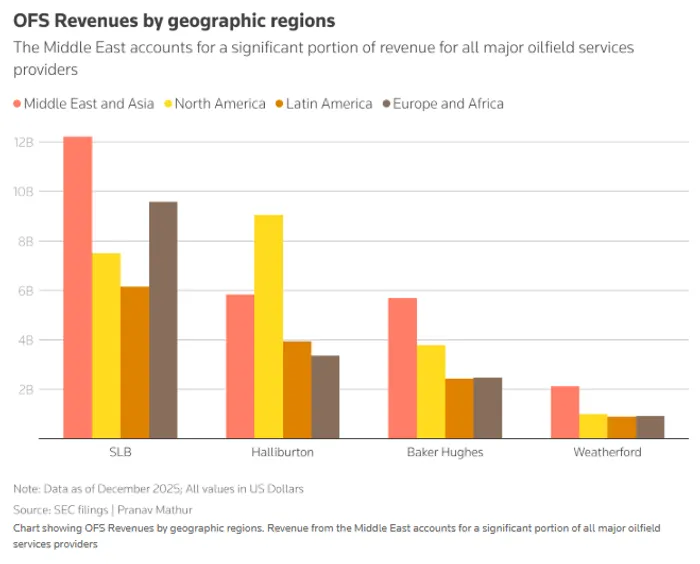

Halliburton (HAL): Energy Cycle Leverage with Emerging Demand Reacceleration

Halliburton sits at the center of the global oilfield services ecosystem, and current conditions suggest an inflection point forming beneath the surface. Despite geopolitical disruptions in the Middle East, the company delivered earnings above expectations—driven by resilient demand in Latin America and Europe. This geographic diversification is increasingly critical in a fragmented energy landscape.

The more important signal is forward-looking: management is observing early signs of North American activity recovery. This matters because U.S. shale remains the marginal supply driver globally. As oil prices rise—partly due to geopolitical tensions involving Iran—producers regain incentive to increase drilling activity, directly benefiting service providers like Halliburton.

Jefferies’ price target increase to $47 reinforces a broader institutional view: the market is underestimating the earnings torque embedded in HAL’s model. Oilfield services companies typically exhibit nonlinear upside—small increases in rig count can drive disproportionately large profit expansion due to operating leverage.

From a valuation perspective, HAL remains attractive relative to historical cycle peaks, particularly given improved capital discipline across the energy sector. Unlike prior cycles, producers are prioritizing returns over volume growth, which stabilizes service demand and reduces boom-bust volatility.

Verdict: HAL offers leveraged exposure to an early-stage energy upcycle, with significant upside if North American activity continues to recover.

Commercial Metals Company (CMC): Structural Demand Meets Institutional Accumulation

Commercial Metals is a less obvious but increasingly compelling play on global infrastructure and construction cycles. The reported stake by Vanguard—nearly 5.8 million shares—signals growing institutional confidence, often a precursor to broader market recognition.

CMC’s core strength lies in its vertically integrated model, spanning scrap recycling to finished steel products. This structure not only enhances margin control but also aligns with sustainability trends, as recycled steel becomes a preferred input in low-carbon construction.

Demand dynamics remain favorable. Infrastructure spending—particularly in North America and parts of Europe—continues to support long steel consumption. Unlike flat steel producers tied heavily to industrial cycles, CMC benefits from public sector-driven demand, which tends to be more stable and policy-backed.

Financially, the company maintains a strong balance sheet with disciplined capital allocation. Free cash flow generation has been consistent, enabling both reinvestment and shareholder returns. Compared to peers, CMC trades at a reasonable multiple, especially considering its margin resilience and structural tailwinds.

The key upside catalyst lies in pricing stability combined with volume growth. If construction activity remains steady while input costs (scrap) stay controlled, margins could expand further.

Verdict: CMC is a quietly compounding industrial name with institutional support, offering a balanced mix of cyclical exposure and structural demand stability.