Top Rated Stocks: This Software Stock Surged 30% After Blockbuster Q1 Results

One AI software winner just delivered a massive beat and raised guidance sharply. Meanwhile, booming data center demand is tightening aluminum supply, while a beverage giant’s turnaround strategy is finally starting to work.

Datadog Inc (DDOG): Surged 30% After a Strong Q1, AI Monetization Is Turning Hypergrowth Into Reality

Datadog delivered one of the strongest enterprise software earnings reports of the year, reinforcing the market’s growing preference for companies that can not only participate in AI infrastructure spending, but clearly monetize it.

First-quarter revenue reached $1.07 billion, significantly ahead of the $1.02 billion consensus estimate, while adjusted EPS of $0.51 also topped expectations.

The real surprise came from guidance. Management sharply increased fiscal 2026 revenue guidance to $4.30-$4.34 billion from the previous $4.06-$4.10 billion range. Adjusted EPS guidance was also raised materially to $2.36-$2.44 from $2.08-$2.16.

The stock surged 31% following the release, signaling that investors believe the company’s AI-driven growth acceleration is sustainable rather than temporary.

CEO Olivier Pomel revealed that Datadog secured two major hyperscaler customers tied to superintelligence training labs. This matters because hyperscaler AI spending increasingly represents the highest-quality enterprise demand in technology markets. These clients require massive observability, cloud monitoring, and infrastructure optimization capabilities, placing Datadog directly within the AI infrastructure stack.

The underlying metrics were equally impressive. Quarterly bookings jumped 37% to $1.03 billion, while remaining performance obligations surged 51% to $3.48 billion. CFO David Obstler also noted that strong trends continued into April, easing fears that enterprise AI demand may be slowing.

Wall Street reacted aggressively. TD Securities described the quarter as an “eye-popping print” and labeled Datadog a “must-own stock,” while Guggenheim raised its price target to $225.

Datadog’s combination of AI-native infrastructure exposure and visible monetization pathways currently places it among the strongest-positioned enterprise software companies in the market.

Alcoa Corp (AA): AI Data Centers Are Creating a Structural Aluminum Story

Alcoa is increasingly transforming from a cyclical commodity producer into a strategic AI infrastructure supplier. While investors remain focused on semiconductors and data centers themselves, a less appreciated bottleneck is emerging: the enormous amount of aluminum required to support power infrastructure, electrical systems, and industrial expansion tied to AI.

Aluminum prices have already climbed above $3,100 per metric ton, versus roughly $2,600 a year ago.

CEO William Oplinger stated that Alcoa is actively supplying AI data centers, while rapidly rising electricity demand is tightening aluminum markets globally. JPMorgan previously forecast a roughly 2 million metric ton aluminum deficit by 2026, suggesting structural rather than temporary supply tightness.

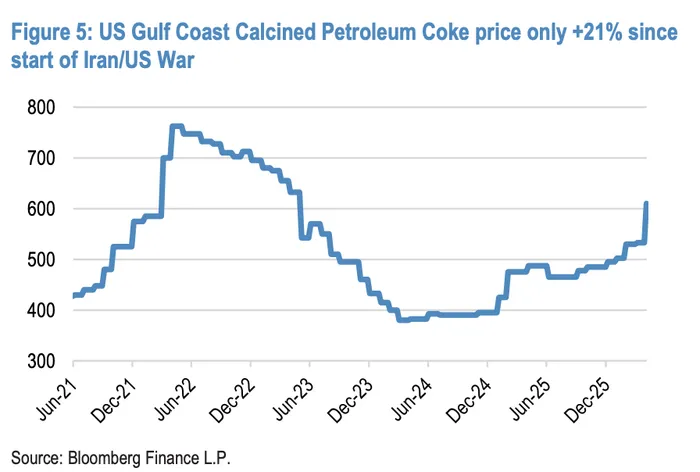

Yet key upstream materials remain underpriced relative to broader energy markets. JPMorgan noted that calcined petroleum coke—a critical aluminum production input—has risen only 21% over the past year, far below the surge in Brent crude and jet fuel prices. This suggests additional cost inflation risk may not yet be fully reflected in aluminum pricing.

Geopolitical factors are also amplifying supply concerns. Roughly 20% of global calcined petroleum exposure is directly tied to the Strait of Hormuz region, meaning prolonged Middle East disruptions could further tighten supply chains.

Operational execution remains another strength. Oplinger emphasized the company’s ability to maintain stable supply chains despite disruptions ranging from Middle East tensions to Cyclone Narelle in Western Australia.

Financial performance is already improving sharply. First-quarter net income reached $425 million, roughly double the prior-year level of $213 million.

The key thesis is straightforward: AI infrastructure expansion is not just a semiconductor story—it is also an industrial materials story. Alcoa may be positioned at the center of that trend.

PepsiCo Inc (PEP): Pricing Reset and Health Trends Are Reviving Growth

PepsiCo’s latest quarter suggests the company may be entering the early stages of a meaningful operational recovery. After facing pressure from slowing consumer demand and pricing fatigue, management appears to be successfully recalibrating its strategy through targeted price reductions and healthier product positioning.

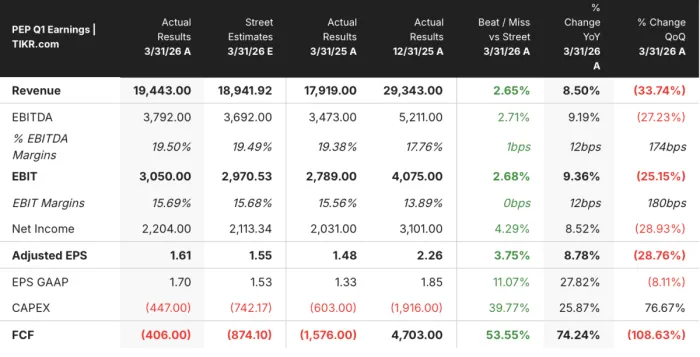

CEO Ramon Laguarta implemented price cuts of up to 15% across several major snack brands. The impact became immediately visible. North American food unit purchase frequency increased by roughly 300 million transactions, while organic sales growth improved from a 1% decline in the prior quarter to 2% growth this quarter. This strongly suggests consumers are responding positively to the company’s pricing adjustments.

Importantly, PepsiCo is also adapting to shifting consumer preferences toward healthier and less processed foods. The company introduced higher-fiber and higher-protein product offerings while reshaping its portfolio mix to align with evolving demand patterns.

Gatorade’s broader transformation may prove especially important. PepsiCo is launching lower-sugar, better-hydration product lines while removing artificial coloring from powdered and ready-to-drink offerings. Its upcoming “Gatorlyte Longer Lasting” product targets athletic and outdoor consumers through enhanced electrolyte functionality.

Management also emphasized cost stability. CFO Steve Schmitt noted that PepsiCo’s commodity hedging programs should help offset ongoing inflationary pressures and provide near-term earnings visibility.

Perhaps the most important signal was management’s decision to reaffirm full-year guidance for 2%-4% organic revenue growth and 4%-6% core constant-currency EPS growth. This indicates confidence that first-quarter improvements were not merely temporary.

In an environment where many consumer companies continue struggling with demand softness, PepsiCo’s combination of pricing discipline, health-focused innovation, and operational scale may position it for a steadier recovery than investors currently expect.