Cerebras IPO Could Still Be a 100%+ Opportunity as a Richly Valued Nvidia Challenger, With OpenAI and AWS Just the Beginning

With the AI frenzy continuing and stocks hitting record highs, the IPO market could finally regain momentum before SpaceX goes public. Cerebras Systems, the rising "next Nvidia" AI processor company backed by OpenAI and Amazon Web Services, is set to begin trading on May 14 under the ticker "CBRS." While Nvidia currently dominates AI training, Cerebras is positioning itself as the fastest inference infrastructure provider in the world, especially as inference becomes increasingly important for real-world AI adoption. Of course, the stock already carries an aggressive premium valuation, but its massive potential and improving long-term outlook could still suggest meaningful upside if the AI rally continues.

The offering is being led by Morgan Stanley, Citigroup, Barclays, and UBS, signaling strong institutional interest. The IPO price range has already been raised to between $150 and $160 per share, with valuation of roughly $32 billion, implying a price-to-sales ratio of 63x based on projected 2025 revenue, as investors rush to board the "next Nvidia" trade.

The Fastest Inference Processor in the World, but Not Without Disadvantages

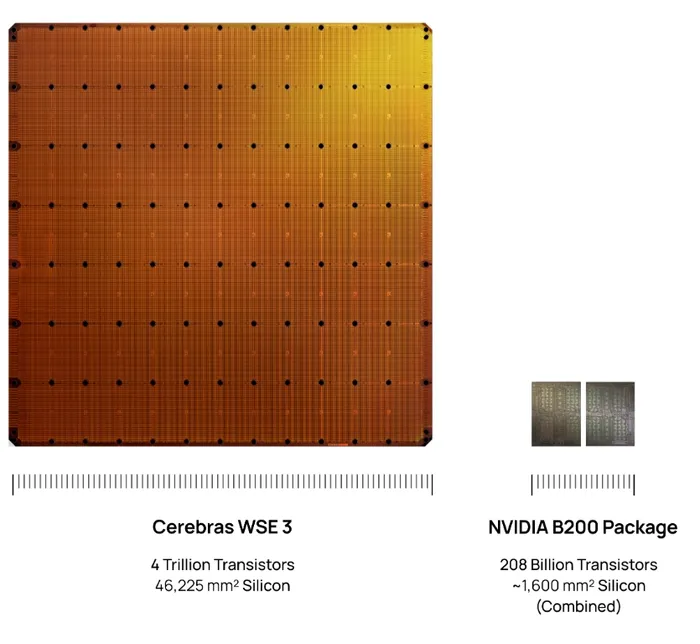

Founded in 2016, Cerebras is a Sunnyvale-based pioneer focused on solving the "interconnect bottleneck" that limits modern AI clusters. Unlike traditional chipmakers such as Nvidia or AMD, which cut silicon wafers into smaller chips and connect them with high-speed cables, Cerebras turns the entire wafer into a single giant processor known as the Wafer-Scale Engine. Built using TSMC's 5nm process, it is currently the largest chip ever produced.

AI computing generally depends on two core elements: processing power and memory bandwidth. With 4 trillion transistors and 900,000 AI-optimized cores, the WSE-3 is 58 times larger than Nvidia's B200 chip. It also contains 19 times more transistors and delivers 2,625 times more memory bandwidth than Nvidia's B200 package, which itself contains two separate chips.

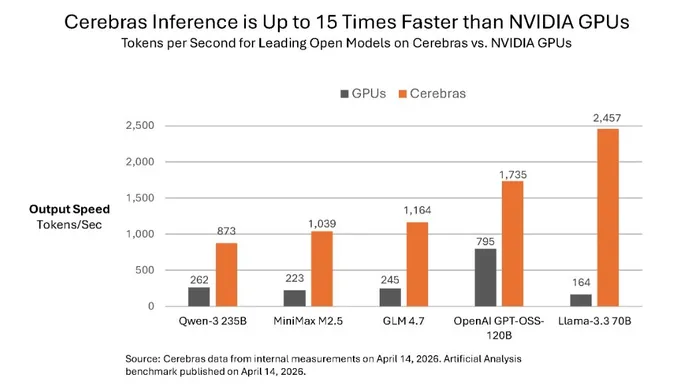

That enormous memory bandwidth gives Cerebras a major advantage in inference workloads, which are becoming increasingly important as AI applications move into real-world deployment. Thanks to this bandwidth advantage, AI responses powered by the WSE processor can reportedly run up to 15 times faster than those using Nvidia's B200 on benchmarked open-source models.

However, that does not mean Cerebras is without weaknesses. Nvidia's acquisition of Grok in December showed that the company is also placing greater emphasis on inference. Through vertical integration, Nvidia could eventually dominate both the training and inference markets. In addition, because Cerebras builds processors using entire wafers, the manufacturing process is significantly more complicated and prone to higher defect rates. The systems also come with a steep price tag. A cluster of 45 Cerebras CS-3 systems capable of handling a 1 trillion-parameter model can cost more than $100 million, while an Nvidia GB200 rack may cost closer to $4 million.

So far, Cerebras's customer base has largely been tied to the "Sovereign AI" movement, where countries seek to build independent AI infrastructure. The company's most important partnership has been with G42 and Mohamed bin Zayed University of Artificial Intelligence, which led to the deployment of Condor Galaxy, one of the world's fastest AI supercomputers.

Yet the company's most exciting strategic partnerships arrived this year. Cerebras announced a multi-year deal with OpenAI reportedly worth more than $20 billion. Under the agreement, OpenAI plans to deploy 750 megawatts of Cerebras's high-speed AI compute infrastructure, co-design future models optimized for Cerebras hardware, acquire a minority stake in the company, and potentially contribute another $1 billion toward data center development. Meanwhile, Cerebras also signed a partnership with AWS, becoming the first hyperscaler to deploy Cerebras systems inside its data centers while integrating them with AWS's Trainium 3 chips to accelerate inference workloads.

These partnerships could become an early signal that hyperscalers are increasingly willing to diversify away from Nvidia. Companies such as Alphabet, Microsoft, and Meta are already working with Broadcom on custom ASIC solutions. That trend could ultimately benefit Cerebras as well, especially after Nvidia's move deeper into inference infrastructure.

Financials

Since Cerebras only updated its financial outlook through 2025, visibility into 2026 remains limited. Still, the current numbers provide a useful glimpse into the company's trajectory.

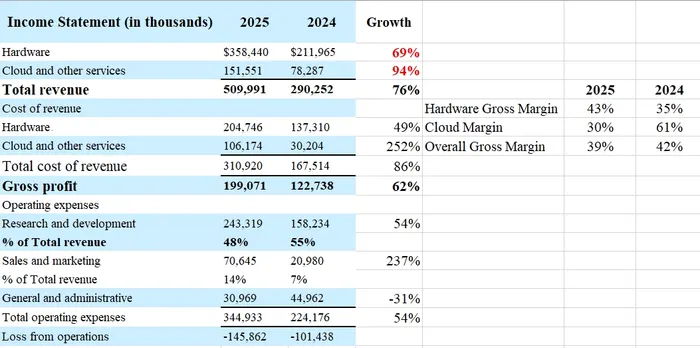

For the full year, Cerebras reported revenue of $510 million, representing 76% year-over-year growth, although the company still posted a net loss of $146 million. Gross margin came in at 39%, down from 42% in 2024.

Revenue can generally be divided into two segments: hardware and cloud services. Hardware revenue includes sales of the CS-3 systems, embedded WSE AI chips, advanced cooling systems, power delivery technology, and networking infrastructure. Cloud revenue comes from providing AI compute access through APIs or through cloud providers such as AWS and Microsoft. In 2025, hardware and cloud generated $358 million and $151 million in revenue, representing year-over-year growth of 69% and 94%, respectively.

There are several notable points here. Hardware and cloud gross margins came in at 43% and 30%, respectively. Hardware margins improved from 35% the previous year, reflecting stronger pricing power, while cloud margins fell sharply from 61% because of rising infrastructure and compute expansion costs. Importantly, the OpenAI agreement will likely contribute heavily to cloud revenue, meaning margins could remain under pressure. For comparison, Nvidia currently maintains gross margins near 75%, highlighting the large profitability gap between the two companies.

It is also worth noting that Customer A and Customer B accounted for 62% and 24% of total revenue in 2025, respectively. Those customers are likely G42 and MBZUAI, underscoring Cerebras's heavy dependence on a small number of major clients. While that concentration risk is significant, it is also somewhat expected in the current AI infrastructure race. More importantly, the company's existing financials do not yet fully reflect the contributions from OpenAI or AWS, leaving room for a potentially stronger forward outlook.

Cerebras has also been aggressively investing in research and development. R&D expenses accounted for 48% of total revenue in 2025, compared with roughly 8% for Nvidia and 23% for AMD. That massive spending reflects the company's focus on building technologically differentiated products. Meanwhile, sales and marketing expenses surged 237% to $70.6 million as Cerebras accelerated efforts to expand its commercial presence.

Valuation

At a $32 billion valuation, Cerebras would trade at roughly 63 times projected 2025 revenue, which would clearly make the stock appear extremely expensive on the surface. However, those financials still do not fully incorporate the impact of the OpenAI and AWS partnerships, while additional hyperscaler customers could eventually join the ecosystem, including potential opportunities with Anthropic, Meta, or Google Cloud.

We can attempt a rough projection for 2026 revenue based on current assumptions. If the company maintains 50% organic revenue growth from its existing customer base, which may still be conservative given the ongoing AI boom, while also recognizing OpenAI's $20 billion commitment over three years, Cerebras could potentially generate around $7.7 billion in annual revenue this year before even accounting for incremental contributions from Amazon. Under that scenario, the company's price-to-sales ratio could quickly compress to roughly 4.15x.

For comparison, the average price-to-sales ratio among major AI chip companies based on annualized quarterly revenue currently sits closer to 19x, implying that Cerebras could eventually trade at a much higher valuation if execution remains strong. Of course, those projections assume OpenAI pays close to full contract value, which still carries uncertainty given OpenAI's own cash flow challenges.

A more balanced benchmark may be a 15x P/S ratio. Assuming OpenAI contributes only 60% of its annual commitment this year while the existing business still grows 50%, Cerebras could reasonably justify a valuation closer to $74.4 billion, roughly 123% above the current IPO valuation. Importantly, this estimate still excludes any meaningful contribution from AWS or future hyperscaler adoption. As a result, the company's fair valuation range could potentially land between $74 billion and $100 billion, although that would still represent an aggressive premium for a startup operating in an increasingly competitive market.

Ultimately, Cerebras remains one of the highest-risk but also potentially highest-reward AI IPOs in recent years. The company is still far behind Nvidia in scale, profitability, ecosystem strength, and customer diversification, while its technology comes with meaningful manufacturing and execution risks. However, its unique positioning in inference acceleration, combined with growing support from OpenAI, AWS, and sovereign AI projects, gives Cerebras a realistic path to becoming a major infrastructure player in the next phase of AI adoption. If the AI boom continues and inference demand expands as expected, the stock could still deliver substantial upside despite its already elevated valuation.