Top Rated Stock: Fear the AI Bubble? Look Beyond Semis

AI is reshaping online shopping, obesity drugs remain a massive growth market, consumer demand is stabilizing, and rising liquidity could push Bitcoin even higher.

HERE ARE OUR PICKS FOR THIS WEEK!

----------------------------------------------------------

Amazon.com Inc (AMZN): AI Shopping Could Unlock the Next Consumer Platform Shift

Amazon is quietly positioning itself to dominate the next phase of AI-driven commerce.

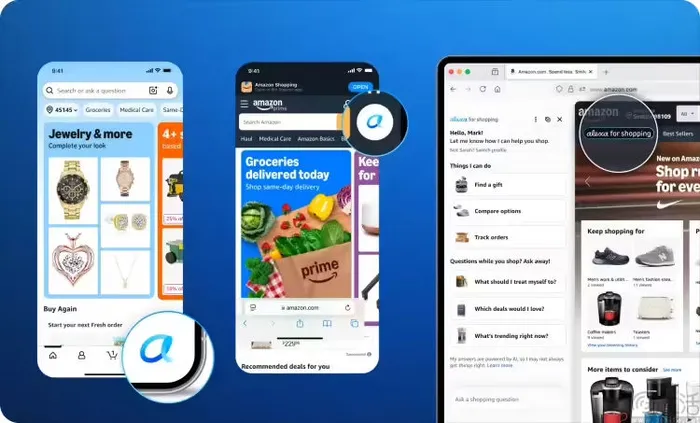

The company’s new “Alexa for Shopping” initiative represents far more than a simple upgrade to its existing Rufus assistant—it is an attempt to create a deeply personalized AI commerce ecosystem that combines product intelligence, behavioral targeting, and cross-platform contextual awareness.

The most important strategic shift is Amazon’s decision to integrate Rufus’ product expertise with Alexa+ personalization and broader web-wide information gathering. Unlike traditional search-driven shopping experiences, Amazon is moving toward an agentic AI model capable of proactively understanding user intent, spending behavior, and purchasing patterns.

The platform’s capabilities are significant. Users can search products using photos, track discounts based on browsing and shopping history, compare products, review price history, and automate recurring purchases. More importantly, Amazon is introducing conditional shopping logic. Consumers can instruct Alexa to buy products only under highly customized scenarios—for example, only adding sunscreen to a cart if the price falls below $10 and no purchase has been made within the past two months.

Cross-device continuity may become Amazon’s hidden competitive advantage. Conversations initiated on Echo devices can seamlessly carry into Amazon’s website ecosystem, creating a persistent AI shopping assistant that remembers context across sessions and devices.

Meanwhile, Amazon is also expanding beyond retail. The upgrade from “Supply Chain by Amazon” to “Amazon Supply Chain Services” opens the company’s logistics infrastructure to businesses of all sizes, including non-Amazon sellers. This effectively positions Amazon as a broader enterprise logistics and fulfillment platform.

The long-term implication is critical: Amazon is evolving from an e-commerce marketplace into an AI-powered consumer operating system. If successful, this could materially strengthen customer retention, increase purchase frequency, and deepen monetization across retail, advertising, and logistics.

Pfizer Inc (PFE): Obesity Pipeline Could Redefine the Next Decade

Pfizer’s latest earnings report suggests the company may finally be stabilizing after the post-pandemic collapse in Covid-related revenue. First-quarter adjusted EPS came in at $0.75, ahead of expectations for $0.72, while revenue reached $14.45 billion versus the $13.79 billion consensus estimate.

The market’s focus is increasingly shifting away from declining Covid product sales and toward Pfizer’s next growth engine: obesity treatments and next-generation pipeline expansion.

CFO Dave Denton recently emphasized that newly launched and acquired products should support growth through the end of the decade, partially offsetting losses from older drug declines. That statement matters because investors have been searching for evidence that Pfizer can successfully replace fading pandemic-era revenue streams.

The centerpiece of this transition is Pfizer’s aggressive investment in obesity treatments, including its recent $10 billion acquisition of obesity biotech Metsera. The obesity drug market is rapidly becoming one of the largest pharmaceutical opportunities globally, with long-term market estimates reaching hundreds of billions of dollars.

Pfizer’s strategy is particularly important because it combines internal pipeline development with external acquisitions. This diversified approach reduces binary risk while accelerating participation in the highly competitive weight-loss segment currently dominated by a handful of major players.

Valuation also remains attractive relative to large pharmaceutical peers. Investors continue to discount Pfizer due to concerns over patent expirations and declining Covid revenue, but that pessimism may increasingly overlook the company’s evolving growth profile.

The company’s dividend strength remains another stabilizing factor. Pfizer continues to offer one of the stronger yield profiles among major pharmaceutical companies, providing downside support during periods of sector volatility.

If obesity treatments achieve meaningful commercial success, Pfizer could transition from a post-Covid recovery story into a long-duration growth and income compounder.

Kraft Heinz Co (KHC): Consumer Recovery and Insider Buying Signal a Potential Turnaround

Kraft Heinz may be entering the early stages of a meaningful operational turnaround under new CEO Steve Cahillane. First-quarter sales reached $6.05 billion, comfortably above analyst expectations of $5.89 billion, while adjusted EPS of $0.58 significantly beat the $0.50 consensus estimate.

The strongest signal came from improving demand trends within the US business. For years, Kraft Heinz struggled with sluggish growth, pricing pressure, and changing consumer preferences. However, recent strategic adjustments appear to be stabilizing the business.

Management reaffirmed full-year adjusted EPS guidance between $1.98 and $2.10, roughly in line with Wall Street expectations. More importantly, the company is aggressively investing in brand revitalization and product innovation.

Its “The United Tastes of America” campaign represents the largest portfolio marketing initiative in company history, designed to strengthen emotional brand connection and capitalize on seasonal consumer demand. Limited-time summer-focused product launches are also helping drive incremental engagement across major retail channels.

The insider buying activity may be even more important. SEC filings revealed that director Steve Cahillane purchased approximately 213,100 shares at an average price of $23.46, totaling nearly $5 million. Large insider purchases often signal management confidence in future operational momentum, particularly during turnaround periods.

Kraft Heinz also benefits from defensive characteristics during uncertain macroeconomic conditions. As consumers become increasingly price-sensitive, large packaged food companies with strong distribution networks and established household brands may regain relevance.

Risks remain tied to inflationary pressure, evolving health trends, and competitive intensity. However, if management successfully balances affordability, innovation, and brand engagement, Kraft Heinz could surprise investors who continue viewing the company as a stagnant legacy food business.

MARA Holdings Inc (MARA): Liquidity Expansion Could Ignite the Next Bitcoin Cycle

MARA remains one of the most leveraged public-market vehicles tied to Bitcoin and broader liquidity conditions. The company recently disclosed that it sold approximately $1.5 billion worth of Bitcoin during the quarter to improve liquidity and reduce debt obligations.

While some investors viewed the sales negatively, the move may ultimately strengthen MARA’s balance sheet flexibility ahead of what could become a much larger macro-driven crypto cycle.

The broader thesis increasingly centers on global liquidity expansion. Arthur Hayes, co-founder of BitMEX and CIO of Maelstrom, recently argued that multiple structural forces—including the AI arms race, military escalation, and supply-chain restructuring—are pushing both US and Chinese policymakers toward looser credit conditions.

This matters enormously for Bitcoin. Historically, Bitcoin has demonstrated strong sensitivity to global liquidity cycles and central bank balance sheet expansion. If governments increasingly rely on accommodative financial conditions to support growth and industrial investment, speculative assets could experience another major upward repricing.

MARA’s business model provides amplified exposure to this environment. Unlike directly owning Bitcoin, MARA offers operational leverage through mining infrastructure and treasury holdings. As Bitcoin prices rise, mining profitability and balance-sheet valuation can expand disproportionately.

At the same time, institutional adoption of Bitcoin continues to deepen through ETFs, corporate treasury accumulation, and sovereign-level interest in digital assets.

Risks remain extremely high. Bitcoin volatility, regulatory uncertainty, and energy cost fluctuations can materially impact profitability. However, for investors seeking asymmetric upside tied to a potential liquidity-driven crypto bull market, MARA remains one of the most aggressive publicly traded exposure vehicles available.