Concentration and FOMO Sentiment Continue Pushing the Market to New Highs, but Liquidity Is Flashing Warnings

The stock market continues to reach fresh highs as the AI frenzy persists, with investors consistently eager to buy every dip in chip stocks, the AI narrative primary beneficiaries. Despite the rally, limited market breadth suggests concentration risk is building, which is not favorable for a healthy bull cycle, while the ongoing FOMO mentality could reverse at any moment. Meanwhile, longer term liquidity conditions are beginning to show cracks amid Warsh related uncertainty and rising yields, and those developments deserve close attention.

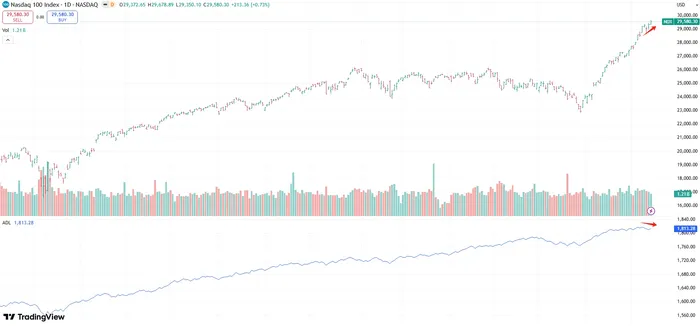

From a technical perspective, the S&P 500 and Nasdaq 100 continue climbing to new highs and remain unwilling to correct, largely driven by the AI boom. The RSI has consistently stayed above 80, reflecting strong bullish momentum without yet reaching an extreme condition. At current levels, however, either another breakout or a pullback could emerge easily, as optimism surrounding AI remains strong while excessive speculation is becoming increasingly concerning.

Volume dynamics also highlight the growing FOMO sentiment. Looking at the S&P 500, recent rally volume has remained near average levels, but trading activity in the Nasdaq 100 has been higher compared with the period before the U.S. and Iran conflict, as investors continue aggressively buying dips in tech, particularly semiconductor related stocks (Micron, Intel, AMD etc). Tech shares are pushing the market to new highs, but concentration risk is also becoming increasingly evident as market breadth narrows. Once the AI driven rally cools even slightly, the correction could become far more severe than expected.

The advance decline line further confirms the heavy concentration within the market. Despite the Nasdaq 100 reaching new highs, the A/D line has drifted slightly lower, suggesting that more stocks have recently declined than advanced. A small group of leading companies is driving the broader indexes higher, which warrants caution because the bullish momentum is not being supported across the broader market.

However, longer term liquidity conditions may require even greater attention. The Fed's balance sheet had been ticking higher during the Middle East tensions even while markets weakened, but recent sessions have started to show signs of softness, mainly due to movements in the Treasury General Account. Long term liquidity remains the foundation of the current bull cycle, and whether that trend can continue should remain a primary focus. As Kevin Warsh emerges as a potential next Fed chair, markets are increasingly considering his preference for combining rate cuts with balance sheet reduction in order to balance monetary policy. With inflation concerns resurfacing because of rising oil prices, Warsh could favor a more aggressive balance sheet reduction in the short term, which would tighten overall financial conditions and weaken longer term liquidity support. That remains a meaningful risk for the market.VBG

The bond market also appears somewhat uneasy. The dollar index has slipped below the 100 level, yet both the U.S. 10 year and 2 year Treasury yields continue rising amid persistent oil price pressure and inflation concerns, even reviving discussion about the possibility of further rate hikes. The spread between the 10 year and 2 year yield remains relatively narrow, although not yet at alarming levels. Sentiment so far remains manageable, but the possibility of tighter financial conditions cannot be ruled out and could become an important short term variable.

Inflation fears and rising yields have also pressured gold. Although the metal remains within a higher low structure, the pattern of descending highs still signals caution. From both a fundamental and technical perspective, including the possibility of delayed rate cuts or even additional tightening alongside potential balance sheet reduction under Warsh, gold no longer appears positioned for the same speculative surge seen earlier this year as rational pricing gradually returns. In contrast, Bitcoin continues trending upward. However, if broader equity sentiment weakens, both assets could come under pressure, making current positioning less attractive in the near term.

Therefore, the market environment is increasingly driven by concentration and FOMO sentiment, with investors continuing to buy dips in chip stocks despite weakening breadth. That imbalance could intensify any future correction once sentiment begins fading, similar to what occurred during the speculative rally in gold. At the same time, longer term liquidity conditions are becoming more concerning, even though liquidity remains the foundation of the broader bull market. An oil driven inflation shock and rising yields could force further balance sheet reduction in order to maintain the current rate structure or potentially allow lower rates later, which may align with Warsh's policy preferences and Trump's broader demands. The market has not yet reached that point, but with equities hovering near historical highs, the storm may be closer and more dangerous than ever.