Quantinuum IPO Could Be the Nvidia Moment for Quantum, With Huge Speculation Potential Despite Sky-High Valuation

With quantum computing emerging from its speculative infancy and the Trump administration pushing funding to accelerate innovation, another heavyweight player is preparing to enter the public markets. Quantinuum is set for its initial public offering on June 4, targeting a valuation of up to $12.7 billion under the ticker symbol "QNT." Positioned at the intersection of theoretical physics and industrial-scale computing, and backed by government support alongside a Nvidia-like ecosystem strategy within quantum computing, Quantinuum has quickly become one of the most closely watched names in deep tech, potentially offering even more speculative upside and trading excitement than the SpaceX IPO. Here is what investors should know about the potential doubling opportunity.

Founded in 2021 through the merger of Honeywell Quantum Solutions and Cambridge Quantum, Quantinuum aims to raise approximately $1.05 billion through the sale of 21.05 million shares. Even after the IPO, Honeywell will remain a dominant force, retaining 49.1% voting control through a dual-class share structure. Investors are essentially buying exposure to the company's technological roadmap while giving up significant governance authority to its parent company.

First, why does quantum computing matter? Quantinuum believes the future of computing will combine CPUs, GPUs, and QPUs, or quantum processing units. While traditional processors excel at general computation and AI acceleration, QPUs are designed to solve problems that become exponentially difficult for classical systems, particularly in physics, chemistry, optimization, and material science. Quantum systems could also generate entirely new forms of data that classical computers cannot simulate efficiently, potentially creating feedback loops that improve future AI training and scientific discovery. In short, quantum computing offers a better framework for simulating real-world systems where traditional computing approaches begin reaching physical limits.

What makes Quantinuum stand out from peers is its full-stack strategy. The company combines high-fidelity trapped-ion hardware with an integrated software ecosystem under its quantum-enabled AI , aiming to solve complex real-world problems in a more commercially applicable way. The ambition is clear: Quantinuum wants to become the Nvidia of quantum computing, following a similar ecosystem-driven model where long-term competitive advantage comes not only from hardware leadership, but also from controlling the software and developer infrastructure powering next-generation computing.

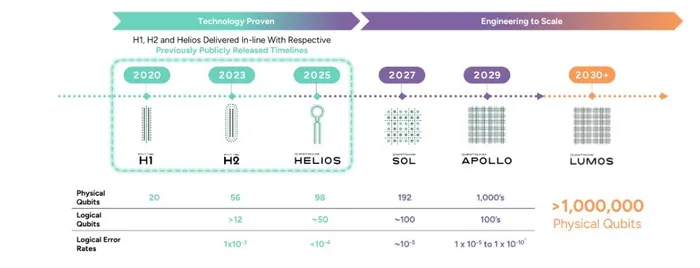

Quantinuum's key differentiation lies not in chasing the highest qubit count or the fastest gate speeds, but in maximizing real-world commercial utility through accuracy, connectivity, and system-level performance. Built on its trapped-ion QCCD architecture, the company has achieved industry-leading fidelity levels, including Helios' 99.921% average two-qubit gate fidelity as of late 2025. It also became the first company to demonstrate logical qubits with higher accuracy than physical qubits, a major breakthrough toward fault-tolerant quantum computing. Rather than focusing solely on headline metrics, Quantinuum emphasizes reducing time-to-solution, which is increasingly viewed as the more meaningful benchmark for practical quantum workloads. The company has already deployed multiple generations of systems, including H1, H2, and Helios, with each iteration improving performance and error correction. Future systems such as Sol and Apollo are expected to scale toward hundreds of logical qubits.

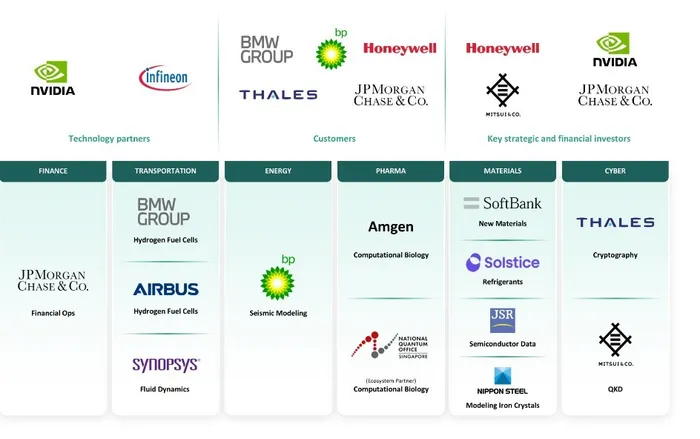

Despite its relatively short standalone operating history, Quantinuum benefits heavily from Honeywell's industrial infrastructure, supply chain access, and enterprise relationships, which could provide a valuable testing ground for applying quantum solutions in real-world industries. Commercialization matters far more than theoretical research alone. The company's stakeholder base is also notable, including Nvidia as both a technology partner and strategic investor, alongside JPMorgan Chase, SoftBank Group, BP, and others. Investors should expect further collaboration between Nvidia and Quantinuum, especially as AI and quantum computing increasingly converge.

In late May, Quantinuum also received a letter of intent from the U.S. government proposing federal funding support for the development of large-scale fault-tolerant trapped-ion quantum computers deemed strategically important to national interests. Combined with the Trump administration's broader $2 billion push toward quantum computing initiatives, Quantinuum could emerge as one of the major beneficiaries, especially given the timing of its IPO. Additional policy-driven catalysts would not be surprising.

That said, despite strong government backing and potential Nvidia partnerships, the company still requires a reality check. Like most quantum peers, Quantinuum remains in the early and heavily loss-making stages of commercialization.

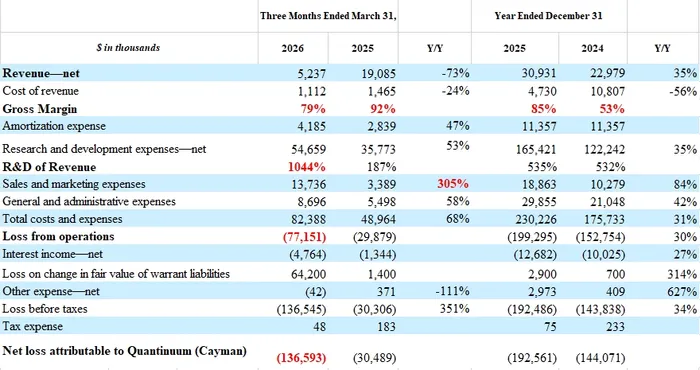

Quantinuum reported $31 million in net revenue during 2025, representing 35% year-over-year growth, while posting a net loss of $192 million. Revenue growth was primarily driven by a $16.5 million specialized quantum hardware transaction tied to a sales-type lease agreement, partially offset by an $8.5 million decline in cloud platform revenue as the same customer transitioned toward hardware deployment. In other words, part of the growth came from shifting revenue mix rather than broad underlying demand acceleration. On the positive side, gross margin reached 85%, highlighting the premium pricing power of its quantum products. However, R&D expenses remained extremely elevated, reaching nearly five times annual revenue due to the capital-intensive nature of quantum development. While that reflects aggressive innovation investment, execution and cost discipline still require further validation. Meanwhile, sales and marketing expenses surged 84% to $19 million in 2025 as the company aggressively promoted itself despite relatively modest revenue growth.

The first quarter of 2026 looked even weaker on the surface. Revenue fell 73% year over year to $5.2 million from $19.1 million in Q1 2025, largely because the prior-year quarter included the one-time $16.5 million hardware transaction. Adjusting for that upfront revenue and normalizing cloud revenue impact, underlying growth likely remained positive at roughly 10% year over year, although still relatively weak. Gross margin declined to 79% from 92% a year earlier, but remained exceptionally strong overall. However, R&D spending surged to $55 million during Q1 alone, exceeding 10 times quarterly revenue as the company accelerated investment into next-generation systems. Sales and marketing expenses also jumped 305% to $8.7 million, continuing the heavy cash burn trend.

The baseline expectation is for spending pressure to remain elevated. Quantinuum's long-term vision centers around achieving "quantum advantage," the point where quantum systems outperform classical computers on commercially meaningful tasks. Reaching that milestone requires continuous aggressive investment across hardware scaling, cryogenic systems, software development, and algorithm design. The challenge is that the timeline for mass-market quantum adoption remains highly uncertain, leaving profitability speculative for the foreseeable future.

Still, relative valuation compared with peers may appear surprisingly attractive.

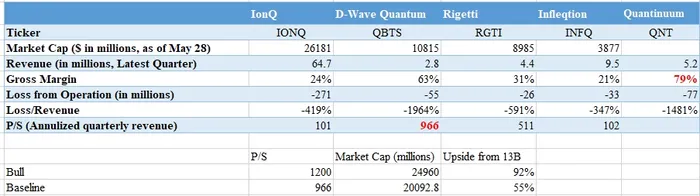

At a $13 billion valuation, Quantinuum would trade at roughly 419 times 2025 revenue and more than 600 times annualized Q1 revenue, an extremely aggressive premium. However, compared with public quantum peers such as IonQ, D-Wave Quantum, Rigetti Computing, and Infleqtion, the valuation still appears relatively plausible within the sector's speculative framework.

D-Wave offers one of the closest comparisons. The company generated just $2.8 million in Q1 revenue while posting a $55 million operating loss and maintaining 63% gross margin, yet still trades near roughly 966 times sales. Quantinuum generated higher revenue, stronger margins, and broader ecosystem positioning, despite similarly elevated losses. If Quantinuum eventually trades at comparable sector premiums, valuation could approach $20 billion, implying roughly 50% upside from IPO pricing. In an extreme bullish scenario driven by AI integration and policy momentum, valuation could potentially approach $25 billion, nearly double the IPO valuation.

Overall, Quantinuum enters the market with one of the strongest strategic backgrounds in the quantum sector. Support from Nvidia, JPMorgan, Honeywell, SoftBank, and the U.S. government creates a credible long-term foundation, while future AI and quantum collaborations could become major catalysts. Fundamentally, the company still remains highly speculative and financially fragile, but relative to other quantum peers, its commercial positioning, pricing power, and ecosystem development appear meaningfully stronger.

Ultimately, Quantinuum represents a high-risk, high-reward bet on the future convergence of AI and quantum computing. The valuation is undeniably aggressive, and the business remains years away from profitability. However, if investors are searching for a potential "Nvidia moment" within the quantum sector, Quantinuum may currently represent one of the closest candidates available in public markets.