UBS Sees Four Tech Stocks With Upside as Market Pricing Diverges From Fundamentals

With the Nasdaq at a record high and valuations already elevated, investors are facing a familiar dilemma: chasing strength feels risky, but sitting out the rally feels just as uncomfortable.

UBS HOLT's latest TMT screen argues that the opportunity has not disappeared. The key is to find companies where market pricing has diverged from fundamental reality.

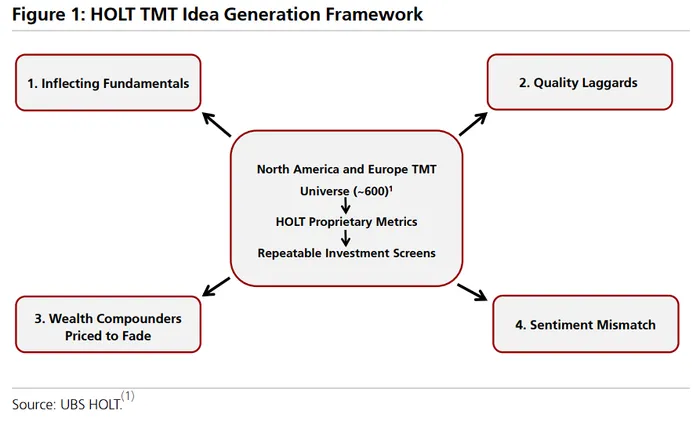

The UBS HOLT team built an objective quantitative framework across about 600 technology and communication-services companies in North America and Europe. The framework identifies four types of investment opportunities: Inflecting Fundamentals, Quality Laggards, Wealth Compounders Priced to Fade, and Sentiment Mismatch.

The screen focuses on cash-flow return on investment, or CFROI, and asset growth. Each category fits a different risk appetite. UBS highlights Broadcom, Accenture, Microsoft and Amphenol as representative stocks, all with Buy ratings.

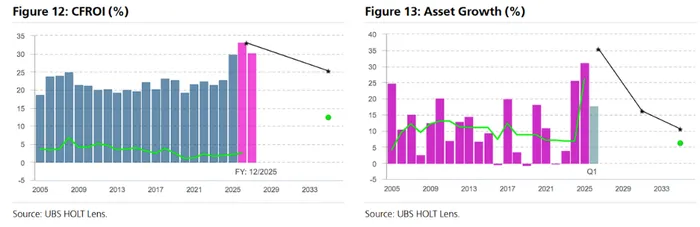

Broadcom: AI Inference Is Driving A CFROI Breakout

At a market high, the cleanest momentum trade is a company whose fundamentals are accelerating.

UBS's Inflecting Fundamentals screen looks for companies whose CFROI is improving faster than peers and whose business momentum is strong. It also excludes stocks that look too expensive versus their own history and peer group. The style is designed for investors seeking accelerating capital returns and strong business momentum.

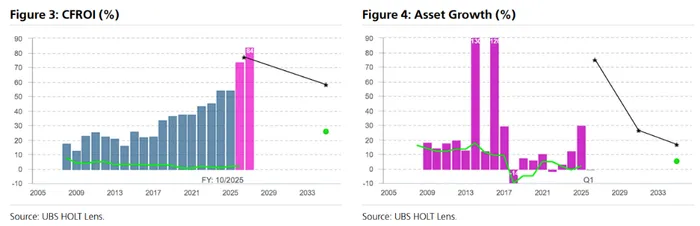

Broadcom is UBS's key example. As inference becomes more important in AI workloads, Broadcom's leadership in ASIC chips is translating into stronger operating performance.

UBS expects Broadcom's 2027 CFROI to exceed 80%. That would rank third across the technology sector and fifth across all global companies.

The market, however, is still pricing Broadcom as if CFROI will revert toward pre-AI levels and asset growth will settle in the mid-single digits. That creates a large gap between implied expectations and fundamentals.

UBS says Broadcom combines high quality, low embedded expectations and very strong momentum. Its CFROI revision is in the 100th percentile among U.S. technology stocks, making it the best-in-class name for this style of trade.

Accenture: Quality Is Selling At A Historic Discount

When capital rushes into the hottest themes, some high-quality companies with durable profitability get sold off too aggressively.

UBS's Quality Laggards screen focuses on companies with forecast CFROI of at least 8%, year-to-date share-price declines of more than 5%, and valuations that sit low versus history. Software and IT consulting names are heavily represented because investors are worried about the long-term impact of AI.

For contrarian investors, this screen is designed as a high-quality bargain list. UBS highlights Accenture as the key case.

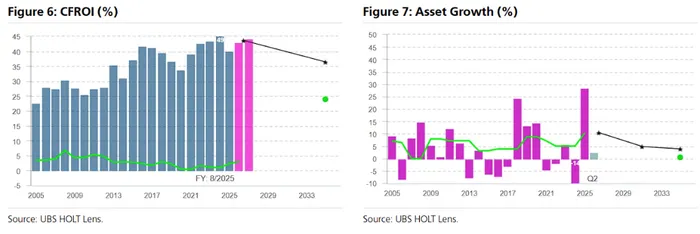

Over the past two decades, Accenture has consistently generated CFROI above 20%. UBS says only 30 companies globally have achieved that record.

Recent consensus forecasts show Accenture's CFROI rising further to nearly 45%. Yet market sentiment has been pressured by concerns that emerging AI models could disintermediate the business and compress margins. The stock is down about 35% year to date.

That pessimism has created a rare valuation setup. On an Economic P/E basis, Accenture's discount to the market is now the widest in its history. On an absolute basis, the stock has only been cheaper during the worst phase of the 2009 financial crisis.

Microsoft: A Compounder Priced For Decay

Some companies are genuine wealth compounders, but the market can still price them as if returns are about to fade.

UBS's Wealth Compounders Priced to Fade screen identifies companies that have delivered high CFROI and high asset growth for years, allowing economic profit to compound at an above-average rate. The mispricing occurs when the market prices in a long-term decline in CFROI.

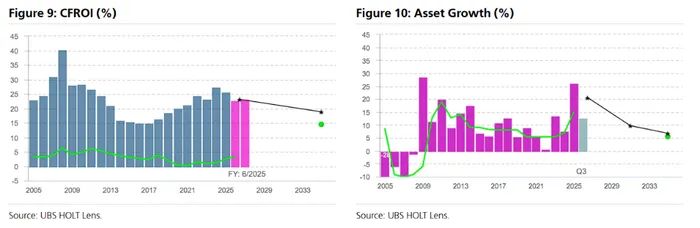

Microsoft fits that profile. UBS says the company has shown sustained operating excellence over the past decade, with CFROI rising from about 15% in 2015 to more than 25% last year.

CFROI is expected to slow in the short term because of higher AI infrastructure investment. But by 2027, Microsoft's economic profit is still expected to increase by more than $25 billion.

That ability to create economic profit has defined Microsoft's value-creation history. Over the past two decades, economic profit has materially declined in only two years.

Despite that record, the market remains skeptical of Microsoft's forecast economic returns. UBS says current pricing implies nearly 900 basis points of long-term CFROI erosion.

That gap between fundamentals and market pricing is why Microsoft falls into the "wealth compounder priced to fade" category.

Amphenol: Estimates Rise While The Stock Falls

When analysts keep raising a company's earnings expectations but the stock keeps falling, the market may be failing to price near-term business momentum.

UBS's Sentiment Mismatch screen looks for companies that have underperformed their regional market by at least 10% over the past quarter while analyst CFROI expectations have been revised higher.

Amphenol is UBS's example. Strong demand from hyperscale cloud customers for high-speed interconnect systems helped the stock rise about 100% in 2025. Yet despite continued and consistent estimate upgrades, the stock is down year to date, reflecting a shift in investor sentiment.

The market is now focused on risk. Investors worry that Amphenol's copper interconnect portfolio could be overtaken by accelerating demand for optical solutions, where the company is still viewed as relatively early in its development.

As the stock has fallen, valuation has become more attractive. UBS says the market-implied CFROI for Amphenol is now at its lowest level in more than three decades. Its Market Implied Yield has reached a historical high, making it one of the most attractive names in technology hardware and equipment.

The Investment Message

UBS's point is not that investors should blindly buy technology stocks after the Nasdaq reaches a record high. The point is that elevated index valuations make security selection more important, not less.

The four buckets offer different ways to define mispricing. Broadcom is a fundamental inflection story. Accenture is a quality laggard trading at an extreme discount. Microsoft is a long-term compounder priced as if returns will fade. Amphenol is a sentiment mismatch where estimates are rising but the stock has weakened.

The common thread is the same: excess return comes from the gap between what the market is pricing and what the fundamentals are doing.