INNIO IPO Could Be the Mini Caterpillar of AI Infrastructure, With Strong Growth Potential but Hidden Risks

With investors chasing AI chips, data centers, and soaring electricity demand, another critical piece of the AI value chain is preparing to enter the public markets. INNIO Group is set to debut on Nasdaq on June 4 under the ticker symbol "INIO," targeting a valuation of up to $20.25 billion. Benefiting from rapid growth in hyperscaler backup power demand and the accelerating buildout of AI infrastructure, INNIO provides energy systems and distributed power solutions that help keep these facilities operating efficiently. As AI-driven electricity consumption continues to surge, the company could emerge as one of the most strategic beneficiaries of the infrastructure boom. However, investors should also pay attention to its hidden risk. Here's what to know.

INNIO is a global energy technology company specializing in industrial reciprocating gas engines that convert gaseous fuels into electricity, heat, and compression services across power grids, data centers, and industrial applications. Following its carve-out from GE's Distributed Power business in 2018, the company, backed by Advent International and ADIA, now operates in approximately 100 countries through its Jenbacher and Waukesha engine platforms. Its manufacturing footprint spans more than 7 million square feet across Austria, the United States, and Canada. Unlike traditional utilities that rely on large centralized power plants, INNIO focuses on localized power generation systems that can be deployed rapidly and operate independently from increasingly strained electrical grids, a capability that is becoming increasingly valuable as AI data center construction accelerates.

AI infrastructure is creating an unprecedented surge in electricity demand. What differentiates INNIO is its ability to dramatically shorten the time-to-power cycle. Its modular behind-the-meter solutions can be deployed in as little as three months, allowing operators to bypass multi-year grid connection delays. The company's Jenbacher engines can start and deliver power within approximately 15 seconds while managing load fluctuations of 25% to 40% without requiring extensive battery support, a critical advantage for AI training and inference workloads that create highly dynamic power demands. INNIO also offers pre-engineered containerized systems capable of scaling up to roughly 25 MW per module, providing customers with plug-and-play deployment, built-in redundancy, and lower implementation risk.

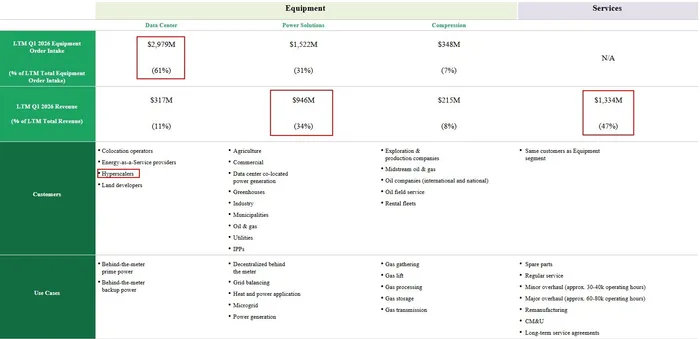

The growth figures speak for themselves. Annual data center equipment order intake surged from just $27 million in 2023 to $2.28 billion by the end of 2025, highlighting explosive demand for AI-related power infrastructure. Momentum continued into 2026, with first-quarter data center equipment orders reaching $1.01 billion, more than tripling from the prior-year period. Approximately 80% of the company's data center backlog is tied to prime power applications, indicating customers increasingly view its systems as core operating infrastructure rather than simple backup solutions. INNIO has already secured several marquee contracts, including an agreement supporting one of the world's largest data center campuses through a multi-gigawatt power plant utilizing its high-efficiency gas engine technology. This could become a major growth catalyst for the company.

Beyond AI, INNIO has spent decades building expertise in gas-based power generation and combined heat and power solutions. Its engine portfolio ranges from 220 kW to 10.6 MW and serves balancing, grid stabilization, CHP, and specialty gas applications. The company is also well positioned for the energy transition, with most Jenbacher platforms capable of operating on hydrogen blends and certain engines already validated to run on 100% hydrogen under AI-driven data center load conditions. Meanwhile, approximately 44 GW of installed capacity supports a highly profitable recurring service business. Given the mission-critical nature of its systems, customers often rely directly on INNIO for maintenance, upgrades, proprietary components, and long-term service agreements that can extend beyond a decade. This creates predictable revenue streams, strong customer retention, and meaningful barriers to entry, while its global service network and leadership in gas compression applications further strengthen its competitive position.

Financially, INNIO presents a very different profile from many recent IPO candidates because it already operates a mature and profitable commercial business.

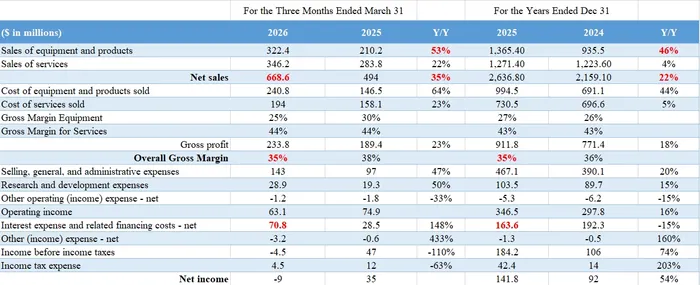

The company generated $2.64 billion in revenue during 2025, representing 22% year-over-year growth, while net income increased 54% to $142 million. Equipment and product sales climbed 46% to $1.37 billion, reflecting robust demand across power generation and data center markets, while the higher-quality service segment grew 4% to $1.27 billion. Overall gross margin eased slightly to 35% from 36% as rapid hardware expansion outpaced the higher-margin service business. Equipment gross margin improved to 27%, while services maintained a strong 43% margin. Although the revenue mix shifted toward lower-margin products, those deployments should create future service opportunities that support long-term recurring revenue growth. The business continues to demonstrate solid pricing power and operational scale, particularly compared with traditional industrial peers.

Notably, SG&A expenses increased only 20% during 2025, slower than revenue growth, while R&D spending rose 15% to $104 million, suggesting management continues investing in future technologies without sacrificing profitability. The largest drag came from interest expenses, which remained elevated at $164 million, reflecting the company's leveraged balance sheet. Nevertheless, INNIO remains solidly profitable, a sharp contrast to many recently listed technology and infrastructure companies that continue to generate significant losses.

The first quarter of 2026 paints a more mixed picture. Revenue accelerated 35% year over year to $669 million, yet the company reported a net loss of $9 million. Growth was primarily driven by a 53% increase in equipment and product sales, supported by strong momentum in data centers, where revenue more than doubled to $107 million, and power solutions, which grew 47% to $168 million. Service revenue increased 22%, suggesting the company is currently benefiting more from new deployments than expansion of its recurring installed base. Gross margin declined to 35% from 38% a year earlier as equipment revenue outpaced the higher-margin services segment. Equipment margins fell to 25%, while service margins remained stable at 44%.

Part of the earnings pressure reflects aggressive expansion efforts. SG&A expenses jumped 47% year over year to $143 million, outpacing revenue growth, while R&D spending increased 50% to $29 million. Those investments remain manageable if execution continues to improve and future growth materializes. However, the more concerning development is interest expense, which surged 148% to $71 million, driven by refinancing costs, higher borrowing expenses, and currency impacts related to U.S. dollar-denominated debt held within euro-based entities.

Overall, INNIO is delivering solid operating performance as a direct beneficiary of the AI infrastructure buildout. Its products address one of the most pressing bottlenecks facing hyperscalers: access to reliable power. As AI training and inference workloads continue consuming enormous amounts of electricity, the ability to deploy efficient generation capacity quickly becomes increasingly valuable. The company also benefits from a powerful combination of hardware growth and recurring service revenue, creating both near-term expansion opportunities and long-term cash flow visibility. However, investors should pay close attention to the balance sheet. Current liabilities stood at approximately $1.6 billion as of March 31, resulting in a current ratio of only 1.32 and an asset-to-liability ratio of roughly 0.96, highlighting elevated financial risk. It is also worth noting that the IPO proceeds will go entirely to existing shareholders, meaning the company itself will not receive any new capital to reduce debt or strengthen liquidity.

Valuation Looks Fair, but the Debt Risk Cannot Be Ignored

At its proposed valuation of roughly $20.3 billion, INNIO trades at approximately 7.6 times annualized revenue based on first-quarter 2026 results. That multiple sits above traditional industrial peers such as Caterpillar at 6.1 times sales, Cummins at 2.8 times, and Generac at 3.9 times. However, INNIO is also delivering significantly stronger growth. First-quarter revenue increased 35% year over year, compared with 22% for Caterpillar, 3% for Cummins, and 12% for Generac.

The premium becomes more understandable when considering the company's positioning within the AI infrastructure buildout. Unlike Caterpillar and Cummins, which remain closely tied to broader industrial and construction cycles, INNIO is rapidly becoming a direct beneficiary of hyperscaler and data center power spending. However, leverage remains a key concern. The company's asset-to-liability ratio of approximately 0.96 trails peers that generally maintain ratios between 1.2 and 1.9, supported by healthier balance sheets and stronger cash generation. Furthermore, because the IPO proceeds are directed entirely to selling shareholders, INNIO will not receive fresh capital. That raises the possibility of future equity issuance to reduce debt, which could create dilution risk for investors.

Even so, the company's exposure to one of the fastest-growing segments of AI infrastructure supports a premium valuation. A price-to-sales multiple of 10 could serve as a reasonable benchmark, implying a valuation of roughly $26.7 billion, or approximately 32% above the IPO valuation. Still, if shares surge significantly after listing, investors may become more focused on execution, margins, and leverage. While the AI infrastructure opportunity remains highly attractive, financial risk should not be overlooked. With numerous AI-related opportunities already available across the market, investors may want to remain selective rather than chase the stock if post-IPO enthusiasm becomes excessive.