Gold Near A Two-Month Low: Buy The Dip Or Prepare For $3,500?

Gold has fallen to its lowest level in more than two months, while silver has suffered an even sharper correction. The long-term precious-metals bull market may not be over, but investors now face a more difficult question: is this a buying opportunity, or could rising rates and weaker demand drive prices much lower first?

Gold’s long-term investment case remains intact, but its short-term outlook has become increasingly dangerous.

As of June 9, spot gold is trading near $4,320 an ounce after touching approximately $4,268, its lowest level since March 23. Silver is trading near $68 an ounce after falling almost 10% during the previous week. The gold-to-silver ratio has climbed to around 63.4, reflecting silver’s sharper correction.

The latest selloff has been driven by a combination of rising Treasury yields, a stronger dollar, weaker physical demand and growing expectations that the Federal Reserve could raise interest rates before the end of 2026.

Yet major banks still expect gold to reach new highs over the longer term. The result is a highly asymmetric setup: gold may eventually trade above $5,000, but investors may need to survive a much deeper correction first.

Gold’s Long-Term Bull Case Survives The Selloff

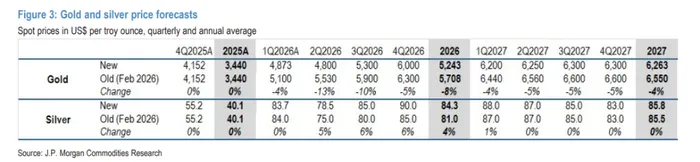

JPMorgan argues that gold’s recent weakness represents a pause rather than the end of the bull market. Its forecasts call for gold to average roughly $5,055 an ounce in the fourth quarter of 2026 and exceed $5,400 during the second half of 2027.

The bank’s bullish outlook rests on sustained demand from central banks and investors.

Central-bank gold purchases are expected to remain around 800 tonnes annually, while investor demand could average approximately 275 tonnes per quarter. Together, these buyers could generate quarterly demand of roughly 585 tonnes, helping offset softer jewelry and industrial consumption caused by higher prices.

The long-term logic remains familiar. Central banks continue diversifying reserves away from the dollar, while investors are seeking protection from geopolitical instability, inflation uncertainty, elevated government debt and concerns over currency credibility.

Citi also remains bullish over the longer term, maintaining a six-to-twelve-month gold target of $5,000 an ounce despite cutting its three-month target from $4,300 to $4,000.

The message from both banks is similar: the structural gold story remains intact, but the path higher may be volatile.

Why Gold Could Fall To $3,500 First

The immediate problem for gold is the rapid shift in interest-rate expectations.

Stronger-than-expected U.S. employment data showed the economy added 172,000 jobs last month. Traders are now pricing a greater than 70% probability of a Federal Reserve rate increase by December, sharply higher than expectations one month ago.

Higher interest rates increase the opportunity cost of holding gold, which generates no income. Rising Treasury yields and a dollar near a two-month high have added further pressure.

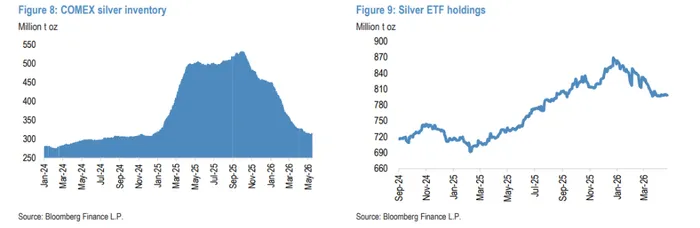

Physical demand is also weakening. High prices have discouraged jewelry buyers and other price-sensitive consumers, while holdings in the world’s largest gold-backed ETF recently declined by 0.5% to approximately 929.6 tonnes.

Energy prices and the Strait of Hormuz remain another major risk.

If the strait remains blocked through the end of summer, elevated energy prices could intensify inflation and strengthen the case for tighter monetary policy. Citi warns that weaker gold purchases under this scenario could push prices toward $3,500 an ounce.

A ceasefire or peace agreement would have mixed consequences. Lower energy prices could reduce inflation and ease pressure on the Federal Reserve to raise rates. However, reduced geopolitical risk would also weaken safe-haven demand for gold.

That leaves the short-term trade vulnerable in either direction. Without renewed physical buying or a clear reduction in rate-hike expectations, gold may struggle to sustain a rebound.

Gold Still Looks Stronger Than Silver

JPMorgan remains constructive on silver prices, forecasting averages of approximately $81 an ounce in 2026 and $85.50 in 2027. However, it is more cautious on silver than gold because silver depends heavily on industrial demand.

Industrial applications account for roughly 60% of global silver consumption. That gives silver greater upside during periods of strong economic growth, but it also makes the metal more vulnerable when manufacturing or technology demand slows.

Solar-panel demand is a particular concern. Manufacturers are reducing the amount of silver used in each panel and developing technologies that substitute cheaper materials. These efficiency gains could weaken one of silver’s most important demand drivers.

China’s silver demand is also expected to fall by approximately 14% year over year, creating another drag on the market.

Earlier in the precious-metals rally, silver looked cheap relative to gold because the gold-to-silver ratio exceeded 90. That argument is now much weaker. With the ratio near 63, silver no longer offers the same obvious relative-value opportunity.

The recent market action reinforces that concern. Gold has fallen to around $4,320, but silver’s sharper decline to roughly $68 has shown how quickly its industrial exposure and higher volatility can amplify losses.

For investors seeking defensive exposure, gold remains the cleaner trade. Silver may offer greater upside during a renewed risk rally, but it also carries more fundamental and cyclical risk.

Buy The Dip Or Wait?

The long-term gold thesis has not broken. Central-bank purchases, reserve diversification and investor demand still support significantly higher prices over the next several years.

But long-term optimism does not remove short-term risk.

Gold is facing higher yields, a stronger dollar, weaker physical demand and rapidly rising expectations of a Federal Reserve rate increase. Under an extended energy and inflation shock, prices could fall toward $3,500 before eventually recovering.

For long-term investors, further weakness may create an opportunity to accumulate gold gradually rather than chase a sudden rebound. For short-term traders, buying the dip without wide stop-loss levels remains risky.

Silver requires even greater caution. Its long-term supply constraints remain supportive, but weakening industrial demand, lower Chinese consumption and reduced solar-panel silver intensity create meaningful headwinds.

The clearest conclusion is that precious metals may still be in a long-term bull market, but the easy trade is over.

Gold remains the preferred defensive asset. Silver remains the higher-risk bet. And investors looking to buy the dip may need to accept that prices could fall further before the long-term rally resumes.